The Indian Auto Consumer Insights Report is a comprehensive report featuring primary and secondary data analytics. The Indian automobile market offers a level playing field for various brands to reach their full potential and enable them to succeed in the market. Automobile brands must have a clear understanding of the economic and cultural mindset of consumers before embarking on any product conceptualization—the points mentioned above serve as a strong underpinning for the cost and product models. The production planning, however, remains the pivotal point in forecasting the overall success ratio in a country like India.

Looking at the year 2021, we observe that the Indian car segment was able to achieve a sales volume of just over 33 lakhs. The Indian PV industry had a fantastic outing in the market, registering a 44% growth compared to 2020. This value corresponds to the sales volume recorded before the COVID-19 pandemic.

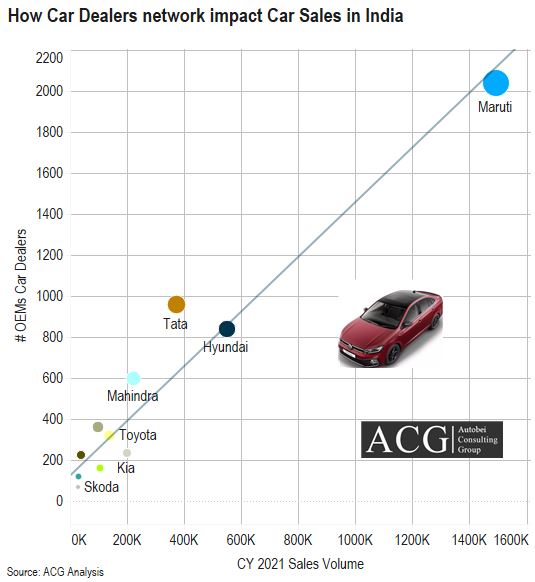

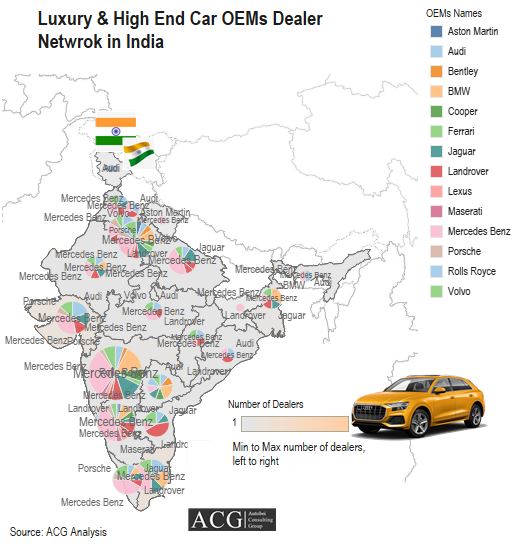

The Dealer network plays a significant role in the OEM’s success in India, enabling it to reach the target segment. There is a direct positive correlation between the number of dealers and the sales volume of Car OEMs:

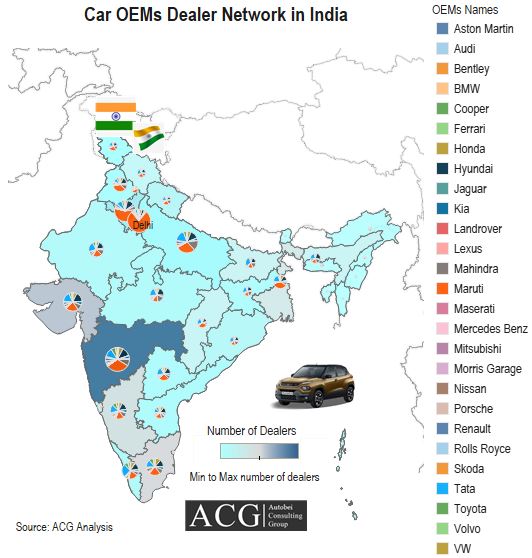

Maharashtra, Gujarat, Delhi. Karnataka and Tamil Nadu arethe top states in terms of the number of car dealers:

Luxury and high-car OEMs have different dealer network strategies due to their target market and buyer segment. Most of them have one or two dealers in a single state, owned by a single firm.

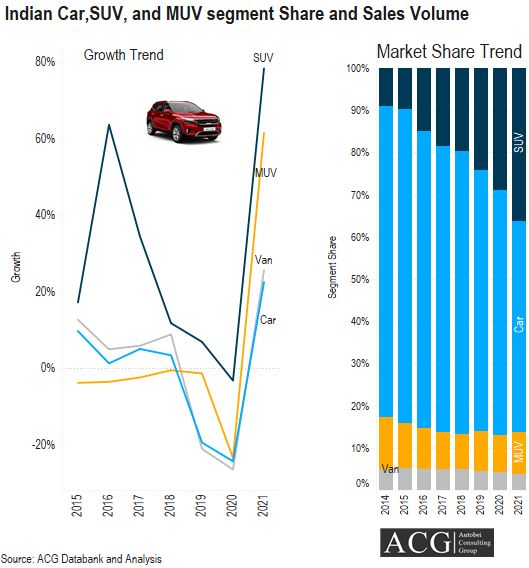

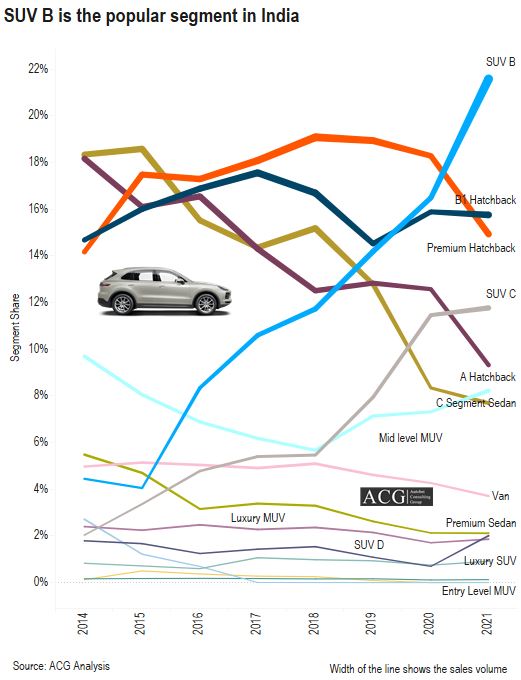

The SUV segment seems to have no stopping at the moment as it has emerged as the first choice for consumers. This is evident from the sales figures, with the volume sold in 2021 more than double that of the previous year.

There was a gradual rise in the overall market share of SUVs; the share was at a meager 9% in 2014 and rose to 37% by 2021. This hurt the overall car segment, as its market share dipped to 50% in the last year from 74%, which was the case in 2014.

The key factor in the rise of SUVs in the contemporary market is the advent of new models alongside a very affordable price range, which caught the buyer’s eye.

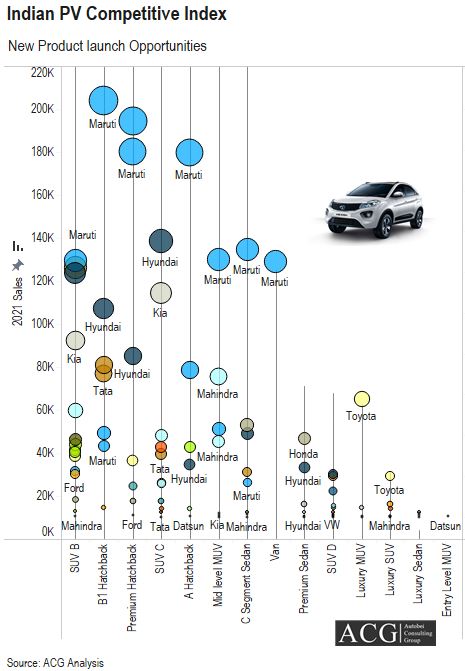

The SUV B has an almost 60% market share in the SUV segment presently, which is 4% higher than the value seen in 2020.

Experts had anticipated a boom in the economic upswing following the COVID period. It’s true that the Indian PV industry has rejuvenated itself over the last few years and has become more oriented towards buyers and product choices. Since the COVID-19 scare is still present across the nation in bits and pieces, one-third of potential buyers are in the process of making up their minds to proceed with the buying choice.

Amidst all the problems faced by the automobile sector of our country, the industry’s future still appears to have a fair chance of excelling in the market, and it indeed has a supreme capacity to grow further. The Indian automobile market is one of the most widely acclaimed market spaces globally and has consistently performed exceedingly well, with demand in this market never falling below the threshold. Indeed, even used vehicles are attracting buyers in the same way as brand-new car models do.

In recent days, the automotive industry has been plagued by numerous problems, presenting formidable hurdles in its path to growth. They are facing a tough time aligning with the digitalization, the advent of electric vehicles, and innovative vehicle connected features, as well as pricing factors. Most importantly, it’s a challenge for them to build a sustainable product that will last for almost half a decade from now. The ongoing tussle between Russia and Ukraine has had an impact on global fuel prices, which will likely lead to significant increases in fuel costs. This, in turn, will affect the pricing of ICE vehicles and overall operations. The advent of electric cars from OEMs would address the issue to some extent, but it can only be a damage control method and never a permanent solution to the problem.

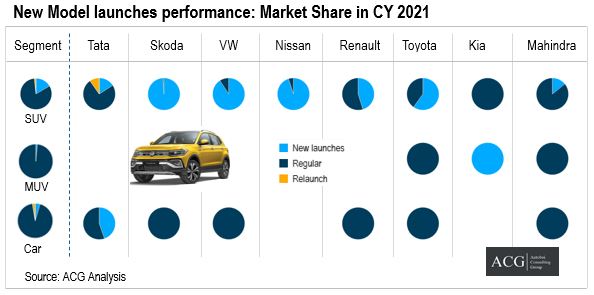

The OEMs have presented new entrants to the market, the count stands at 14 brand new and three reintroduced models, and these new launches have been brought in with a strategy of offering a model as an alternative to the existing market giants, it also aims at bridging the space that exists between the market and also in placing the available products in the key position.

Tata Motors has given an enormous contribution by launching new products at regular intervals. This has set up rigorous competition in the Indian PV industry. Notably, the SUV segment has seen a surge in new entrants, with brands like Kia and Tata demonstrating their potential to capture a significant market share. They can even attract new buyers, potentially causing a dip in sales for other existing brands. The growth recorded in 2021 is immense; the SUV sub-segment saw an overall increase of 90%, while the mid-level MUV segment grew by 43%, and the B1 hatchback segment also grew by 43%. However, SUV D had a fantastic outing in the market, with a magnificent rise in growth of 318% in 2021.

The COVID-19 pandemic has posed a significant threat to the economy, resulting in buyers shifting away from their purchase decisions, especially in the budget range. The manufacturers should continue to focus on the two primary segments: the value-plus segment and the premium segment, as they hold a market share of approximately 85% in the current market scenario.

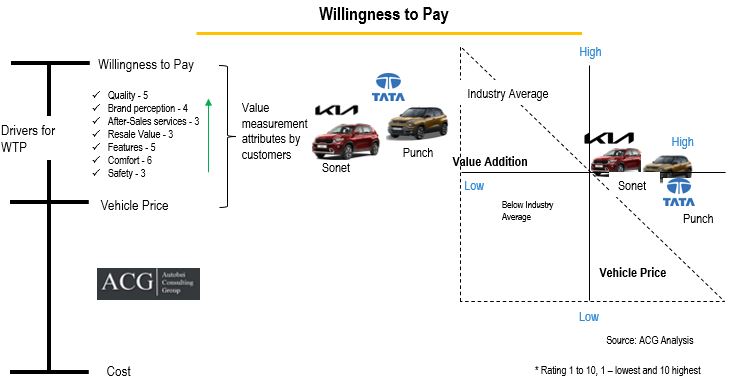

The rise in digitization has had a significant impact on the automotive sector, as customers are now willing to pay a premium for new features in the variant they are purchasing.

The XUV 700 can be seen as a perfect example of this, as buyers are willing to pay a premium price for top-end features. Additionally, we have observed an interconnection between the number of sales that take place at the dealership, which is present across the country. Even the VW Taigun has been the most sought-after by customers due to its solid looks and unparalleled interiors. The Korean brand, Kia, has evolved to be a pivotal contributor in the Indian market, currently ranking 5th in the PV industry in terms of volume, and well placed at position 3rd in terms of revenue generation.

The study, recently concluded by ACG, has shown that buyers are considering even the smallest aspects when making their purchasing decisions, with nearly 5,500 respondents from diverse backgrounds and age groups. We focused on evaluating the vehicle purchase experience of buyers in the top 25 cities in India, which encompassed both urban and rural areas. The survey also aimed to take note of the buyers’ attitudes, their preferences for channels in acquiring information, the choice of product, the cost-effectiveness of the brands, and, most importantly, the service rendered to customers after the sales cycle has ended.

The study has uncovered several key points that will provide the necessary guidance to potential buyers as we embark on the upcoming developmental period in the Indian automobile market.

- The SUV segment aims to conquer the market by offering debut car buyers the opportunity to purchase different variants at an attractive price point.

- There have been various innovative strategies to influence customers’ buying decisions; the best of them has been the venture of offering the “Next best vehicle option.”

- Potential buyers are now shifting their focus to the product they plan to own, rather than just relying on the brand’s reputation.

- The premiums of the car are also valued based on the number of best digital features they have. So the presence of digital features in the care is extremely paramount at this time.

- The rapidly changing market has demanded a change in the used market space. Therefore, employees must now understand what the customer truly expects and deliver it accordingly to ensure a high level of user satisfaction.

The way ahead:

At the moment, the ongoing war between Russia and Ukraine has had an impact on various businesses globally. Once normalcy is restored, oil prices are expected to fall back to their previous level. This would represent a significant breakthrough for the Indian car market. The increasing oil prices will enable a sharp rise in the overall sales of electric cars. The study also concluded that there would be an intense demand for personal cars, and this would take the market a long way ahead. It is also believed that there will be no slowdown in business, and even if there is, it will be easily addressed.

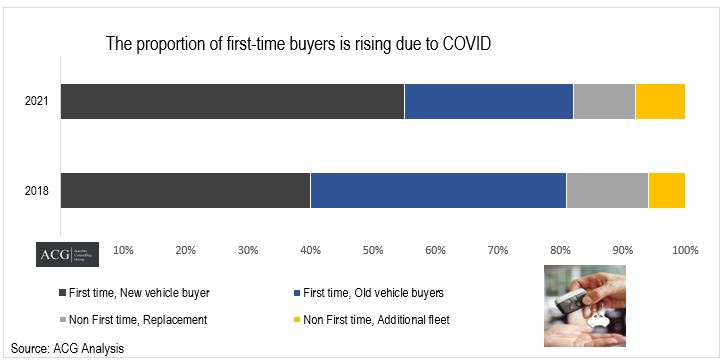

- Debut buyers – new vehicle buyers

- Maiden buyers – Old vehicle buyers

- Non-debut buyers, Replacement

- Non-Maiden buyers, Additional fleet

Increasing demand for the car, SUV, and MUV, and buyers’ eagerness to own a product:

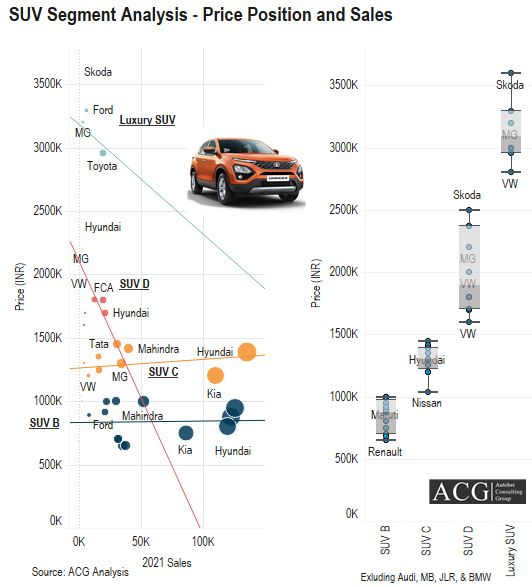

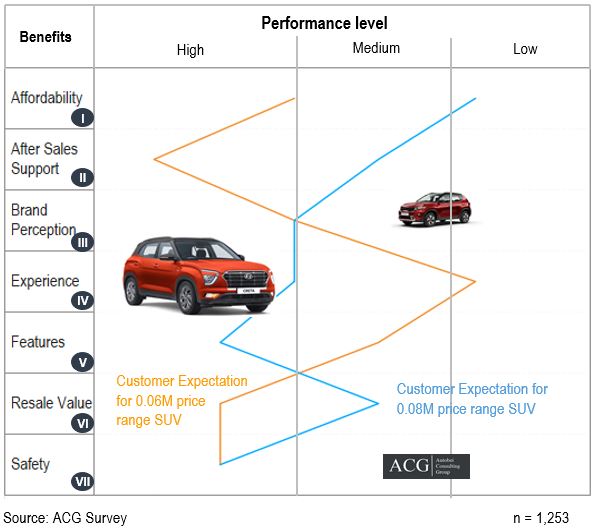

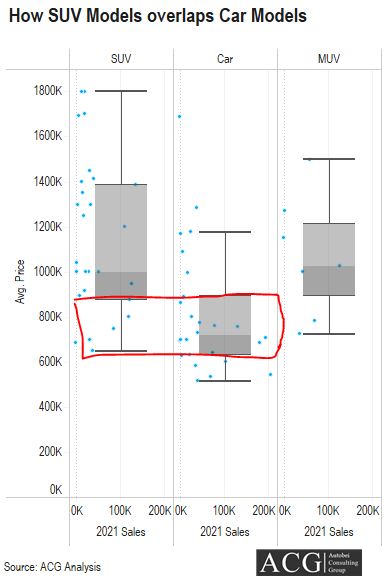

The Indian automobile customers have shown a greater affinity towards owning an SUV, and for this reason, the SUV has become the most sought-after product in the segment. The buyers are looking to own one between the price tags of Rs. 770,000 and 870,700 INR. The study also revealed that almost 22 percent of people mentioned that they are ready to trade up to own a car in the near future. While many even had a wish to go beyond their budget to make a purchase slightly. There were instances where customers claimed that if their existing car were priced between 500,000 and 600,000 INR, then they would never mind going up by a lakh or two to make a purchase of a vehicle with full-fledged features.

The study’s results further stated that SUV models priced between 110,000 INR and 130,000 INR have established an incredible platform for the OEM, and they are indeed making the best use of it. The buyers are looking for vehicles that offer superior performance and render the best cabin and driveability experience.

The overall Market Share held by the SUV B, B1 hatchback, and premium hatchback constitutes almost half of the market presence, with just 27 models available in the market.

Impact of the brand on customers’ buying preferences:

The new launches in the market are doing well, and the brand’s reputation has a significant effect on maintaining the sales performance of these new entrants. It is worth noting that the acceptance rate of new entrants is significantly higher than that of existing models in the market.

Sheer competition in the market space:

The last 3 decades have been challenging for automobile brands. The existing domestic brands and reputable foreign brands are all trying their best to establish a foothold in the market. The contemporary market dynamics are incredibly different from what they were before; now, there has been an increasing demand from debut buyers. The not-so-reputed brands were able to carve out a small space for themselves amidst the presence of globally renowned brands and top-notch domestic brands. However, such a mutual presence would not last long, and only the brands that strike the customer’s aspirations will continue to exist.

In this domestic brand space, the top-performing brands enhanced their value from 13% in 2014 to a massive 18% in 2021. This 5% growth rate in less than a decade is a significant performance factor.

A key point to note from the study is that retention rates, particularly in the Indian automobile market, are at an all-time low. The reason for this needs to be ascertained, but it is clear that the buyers are not returning to the brand for which they had made an earlier purchase. The people who responded that they would purchase a vehicle from the same brand stood at an abysmally low turnout of just 10%. This number slightly increased by 11% and rose to 21% in 2021. Astonishingly, the owners of the car, which is priced at 500,000 INR and above, clearly stated that they are not in favor of making the same brand purchase the next time they plan to upgrade. The people with this opinion stood at 32%. During the period from 2014 to 2021, 53 percent of the people did not turn up for the previous brand they had already owned.

Tata Motors, however, brought about a revolution in the Indian market space by coupling their top-notch innovation with the premium touch to their new SUV and car models. This made Tata Motors the customers’ first choice when considering budget-friendly and premium-feeling cars. Tata Motors has now become synonymous with affordability and a brand that caters to the needs of every customer.

The Indian automobile market is credited with being one of the largest markets for vehicles. The performance of various brands in the Indian automobile market is dependent on several factors, including customer buying preferences, safety, comfort, and many others. Almost 65 percent of the survey participants prefer brands with German roots, while others opted for the renowned JLR (Tata) brand. The study has further revealed that the JLR brand will be well-received by the Indian audience in the future and will gradually evolve to become a pioneer in the luxury vehicle segment. The other foreign brands hailing from South Korea and Germany have caught the customer’s eye and have been successful in creating a prominent name for themselves in the Indian market. If we compare the Indian market with that of China, we see a lack of domestic brands catering to the demand for Luxury vehicles, which has led foreign brands to dominate this segment. The study further indicates that customers are willing to go the extra mile by spending a little more to purchase cars from reputable brands.

There is an entirely different buying behavior and decision-making process for rural and urban Indian customers. In India, the market dynamics that influence buyers’ choices are dependent on numerous factors. Many buyers would rely on the words of their colleagues or those around them when deciding to purchase an automobile for personal use. Apart from this, people also choose to gather relevant data from available internet channels and segregate the brands and products that suit them the most.

There has been a sharp rise in the percentage of people who flock to YouTube and other well-known automobile expert channels and social media handles to discover the best brands and models on the market. The buyer will thus use the obtained information to decide on which specific brand to own. This trend is gradually gaining popularity, and currently, 36 percent of people have utilized such e-services available on the internet. Potential buyers will gather all the relevant information from the sites and then reach out to a sales executive to finalize their choice. At the same time, the other group, which constitutes about 27 percent, is not particularly tech-savvy and won’t rely heavily on the abundant information available on the internet to gather details about the product.

The information obtained from the online and offline modes plays an integral role in influencing the buyer’s mindset. Potential customers avail themselves of all the details about the vehicle’s overall performance, reliability, and technical features. Moreover, buyers tend to go through the blogs and reviews written by existing owners. All these layers together give an initial perception to the potential customer about the choice they would make.

Currently, the market trend is being revised daily in the wake of COVID-19. The most sought-after option by buyers has still been the one where the customer directly visits the showroom and interacts with executives to finalize their purchase. Apart from this, customers are trying to gather as much firsthand information as possible by referring to genuine and popular web pages and other online handles. Customers have already had their expectations set before getting their hands on any model. The prime factors that customers consider when making their buying decisions are the brand’s positioning in the market, exterior aesthetics, premium seating, best-in-class features, and, most importantly, the degree of trust a brand has established over the years, which is also known as the level of customer-centricity.

The key factor to note here is that more than 50 percent of the people believe the internet plays a pivotal role in providing the necessary basic overview for most probable buyers. It is also worth noting that some buyers don’t rely on the internet due to the lack of accurate price information on various portals, which itself is a major hindrance. The pricing of automobiles, especially in the Indian market, varies from state to state, depending on tax slabs and other parameters. This has led to a shift in customer preference from online platforms to offline showrooms, allowing them to determine the actual price and plan for ownership based on their financial feasibility. The male population between the ages of 18 and 40 is the ones who prefer to visit the showroom in person rather than surf the details online. In the current scenario, even the female audience is shifting towards online portals for obtaining details about automobiles before making a purchase. They mostly prefer to use automobile websites and phone applications because of the detailed information and transparency they offer. Even the offline setups are not much behind in this run, as there has also been an increase in visiting the car dealers in person, availing test drives, and getting valuable insights from relatives, friends, and many more; such offline engagements have evolved as the top choice for the potential buyers.

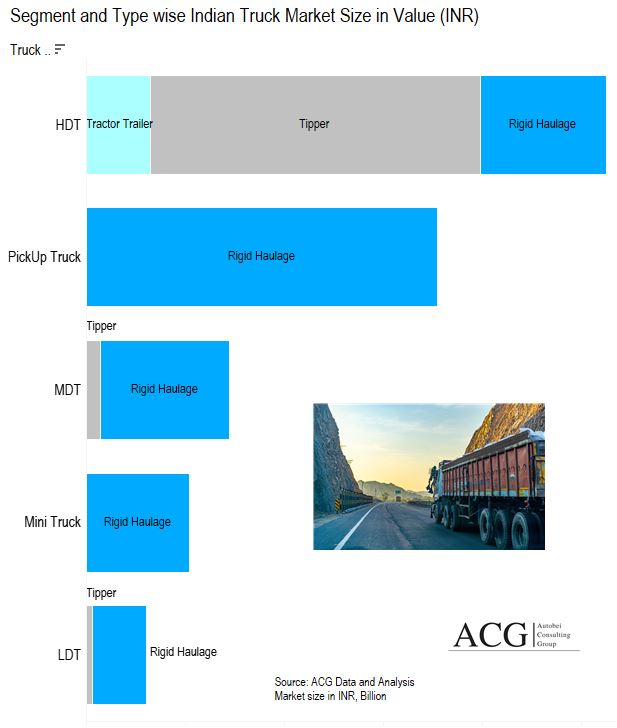

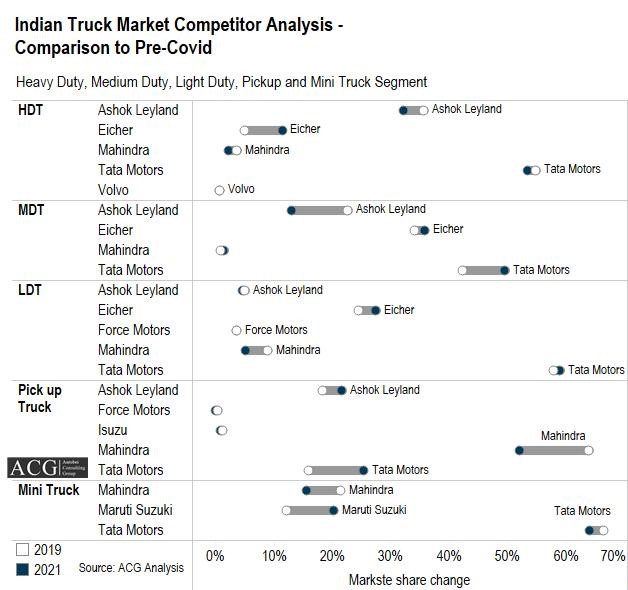

The market dynamics in the MDT segment are very different compared to the other segments we have just discussed. Tata couldn’t continue their uninterrupted streak of exceeding its market hold. Their market share of 80% in the 2nd quarter of 2019 was reduced to a meager 40% by the last quarter of 2021. This segment is now being led by Ashok Leyland as they hold a market share of about 25% currently. It is then closely followed by Eicher, which climbed to this spot by taking over about 8% from its close competitor Tata motors. Overall, Ashok Leyland continues to hold a vital position even in the 10 to 14.5T segment by being able to turn around the overall market presence of 50% and 74% respectively.

The market dynamics in the MDT segment are very different compared to the other segments we have just discussed. Tata couldn’t continue their uninterrupted streak of exceeding its market hold. Their market share of 80% in the 2nd quarter of 2019 was reduced to a meager 40% by the last quarter of 2021. This segment is now being led by Ashok Leyland as they hold a market share of about 25% currently. It is then closely followed by Eicher, which climbed to this spot by taking over about 8% from its close competitor Tata motors. Overall, Ashok Leyland continues to hold a vital position even in the 10 to 14.5T segment by being able to turn around the overall market presence of 50% and 74% respectively.