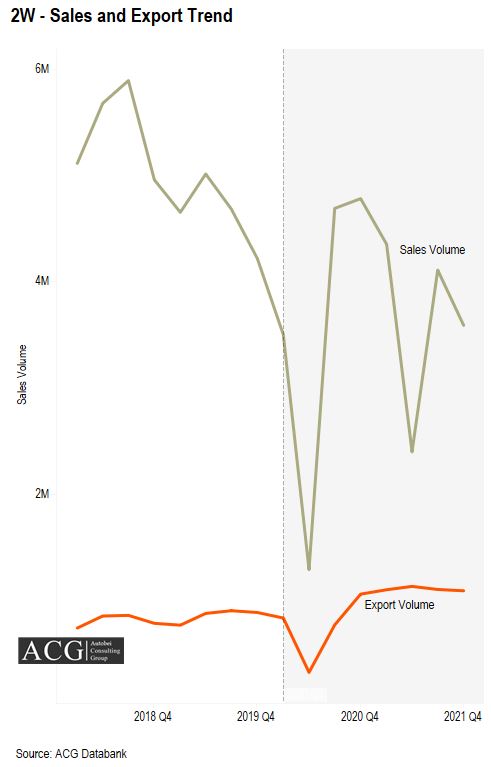

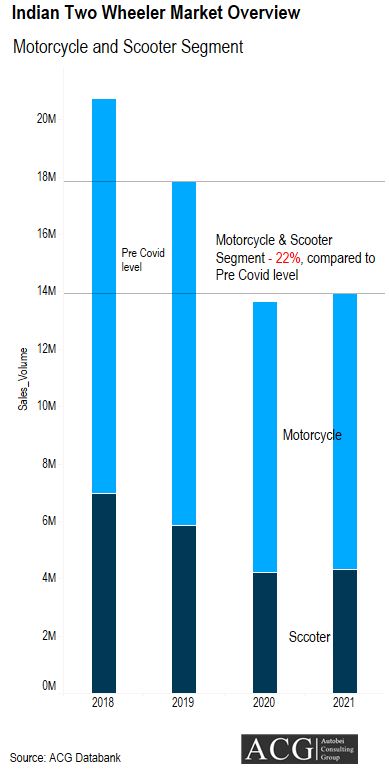

The post-pandemic period unraveled a good growth cycle for the automobile industry specifically for the two-wheeler industry. The statistical analysis underlines that the market shot up by 1.3% in the year 2021 as compared to the year 2020.

However, the industry was able to breathe a sigh of relief as they could reap a good expansion in the export arena by amassing a growth of 48% and 29% in 2020, 2021 respectively. This flawless run of the market was put to a halt in quarter 3 and quarter 4 of 2021 as there was slight degrowth of about 13% for the Scooter vehicle. If this was not the case then the market would have expanded to its ever best.

Brand Position-based on Customer perception: Motorcycle Segment

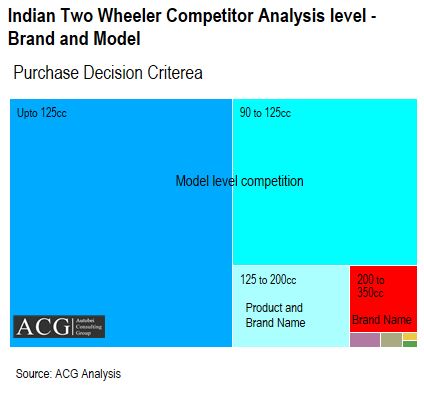

the market dynamics of the two-wheeler segment especially in this segment are very unique because of the customer’s mindset, ever-changing options, and the rise of new entrants in the market.

Brand perception has a big impact on Two Wheeler’s buying decision. We have considered the most important factors in our reprinted sample size like Male, Female, Small towns, metro Cities, Villages, Different professionals, and others.

In our full report, we have published all the attributes which influence customer decisions. Such matrices are useful for OEM’s new product launches and brand strategy.

Bajaj Motorcycle is in the midpoint of Resale Value and Product Reliability.

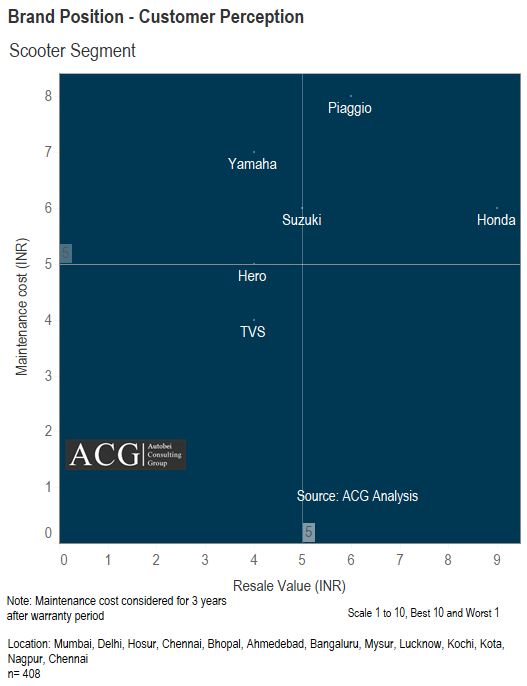

Brand Position-based on Customer perception: Scooter Segment

Brand Position also play important role in buying Scooter. However, the customer preference is different compared to Motorcycle different. Honda is the best in maintenance cost and resale value.

Another point that grab everyone’s attention is that the post COVID performance of the domestic two-wheeler market is slightly better than what it was during the Peak time of the pandemic, but these numbers aren’t even close to what the two-wheeler market was witnessing during its operational year dating back prior to 2020. There was a sharp downfall of the market by almost 22% in comparison to the above.

Indian Two Wheeler Competitor Analysis:

The COVID 19 didn’t really miss out to disrupt the entire market segment and it did have a negative impact during the peak time of its spread. While after this impact, there was a contradicting development in regards to the growth of this OEM segment is concerned.

If we dive deep into the two-wheeler industry then we can see that the motorcycle segment too added strengthened its market space by 1.6%, alongside this was Scooter segment which expanded by 2.7% during the year 2021.

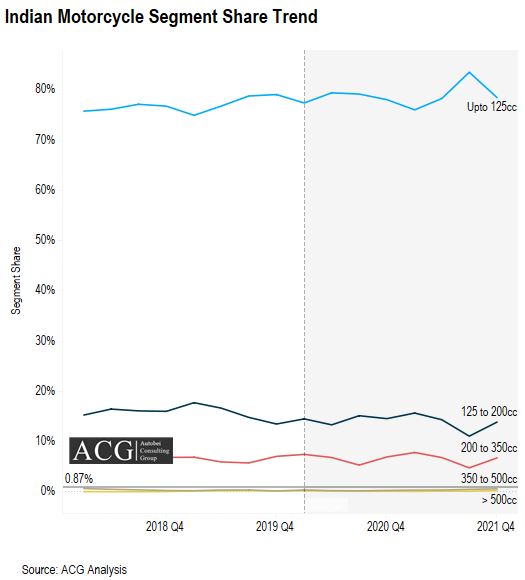

Further, as we try to take a look into the performance of the motorcycle segment, the figures we see are really encouraging and show that this segment has led from the front for the entire two-wheeler industry. The motorcycle segment till the range 125cc got a warm welcome from the customers as it bettered the numbers by adding 2.5% from the previous year. For the range greater than 125cc and less than 200cc the figures show that there was a slight diminish in the growth by about 4.6%. However, for the segment from 200 to 350cc, 350 to 500cc, and above the segment enjoyed an absolute flawless run in the market. The same is evident from the growth figures as the market expanded by 2.1%, whooping 66% and 2% respectively for all the 3 above-mentioned segments.

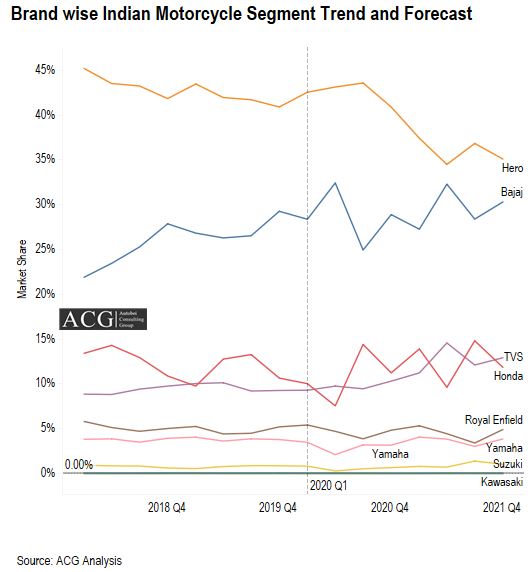

As Hero found it really hard to maintain its consistent performance in the market and even took a bad hit during this period. Its close competitor, Bajaj, however, enjoyed a growth curve at the same time in the budget motorcycle segment. A positive growth curve was also evident from the rise in the overall market hold of Honda and TVS. Astonishingly, Bajaj, which used to stand tall in the market as far as 125cc to 200cc is concerned couldn’t really reap reach dividends during this period as its firm position in the market declined gradually starting from Q1 of 2020. The same was not the case with other players in the market viz. TVS, Honda, and Yamaha as they continued to steer across a potential growth during this period. Another major player in the 350 to 500cc, continued to be an undisputed king of the domestic arena.

The growth curve recorded in the entry-level segment speaks about the exceeding interest in the customers towards various brands of two-wheelers. TVS seemed absolutely no standstill at all in the OEM as it strengthened its base by another 15% in 2021. The fortune even continued to Honda and Yamaha by giving them a major breakthrough and aiding them to grow by 57% and 40% in the last quarter of 2021. The 200 to 350 cc is seen as a premium segment and here Royal Enfield, Honda has always been able to perform to their potential, and even in 2021, they were able to record 42% and 71% in the last quarter of 2021. So overall both these entities did really well despite the hardships and shot up their sales figure exponentially. During Quarter 4 of 2021 for the 500cc and above segment, Royal Enfield and hero recorded amazing numbers and aided them to close the quarter with growth of 125% and 106% in comparison with the 3rd quarter of 2021.

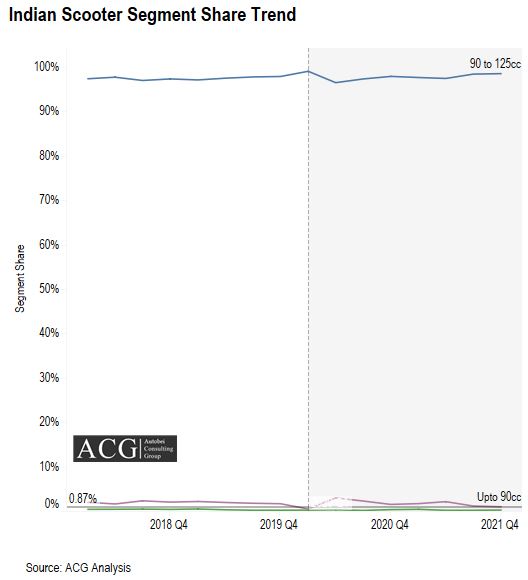

Indian Scooter Segment Share Trend Analysis:

Ever since the rise of geared vehicles the scooter segment has gradually lost its shine in the market. In our detailed report, we have explained why it happened and forecasted this segment. 90 to 125cc is the main segment of the Scooter market.

But the statistics thus observed are quite contradictory to this claim as the scooters of greater than 125 cc stood tall by being able to put across a fantastic growth of 10%. This wasn’t quite applicable for the base variants as they are still not able to put an exciting sales figure to date. Whereas for the 90 to 125cc there was a respectable turn out of about 3% in the year 2021 compared to its previous. Moreover, the growth in 90 to 125 cc is extremely important for the two-wheeler industry as they play a pivotal role in the domestic as well as an export arena.

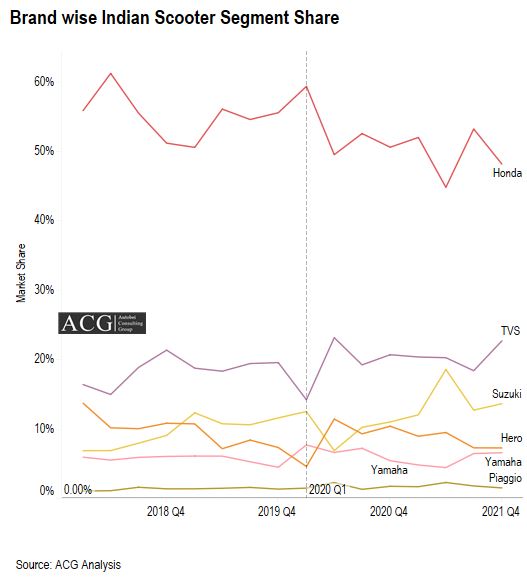

Brand wise Indian Two Wheeler Segment Share Trend and Forecast:

Market leader Honda of the Scooter segment is losing its grip. The TVS and Suzuki are continuously increasing their market share after Covid 19 impact. Piaggio brand became the first choice of premium scooter buyers. The all reasons behind this trend are examined in our detailed report.

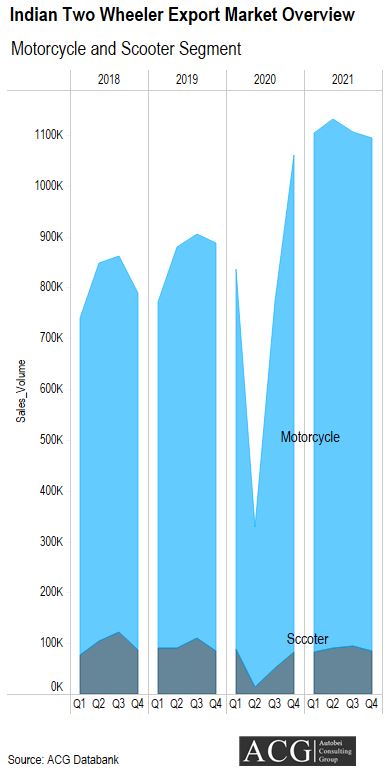

Indian Two Wheeler Export market:

The export market grew by 48% and 29% in 2020 and 2021 compared to the previous year. Two-Wheeler segment export showed excellent growth of 48% in CY 2021. Q3 and Q4 CY 2021 declined export of Motorcycle and Q3 2021 Scooter registered degrowth of 11%.

In spite of the domestic market not handing the required success for the two-wheeler market, the export market came to its rescue and rendered the much-needed breakthrough for this segment. African Nations and a few others in the South Asian region have evolved as the hotspots for the two-wheeler markets. This enables the sales figures in the export category to grow exponentially. The young generation is very much inclined towards owning a two-wheeler that too a sportier one. This trend has served as a boon to the wheeler market while this enabled a substantial rise in the demand for sporty motorcycles and the growth stands at absolute 100% in 2021.

Indian Motorcycle Segment Share Trend and Forecast:

The growth was not just restricted to the sporty models but also expanded for 125 to 200 cc entrants by enabling them a growth potential of 61% and 42% despite the spike in COVID during the year 2021.

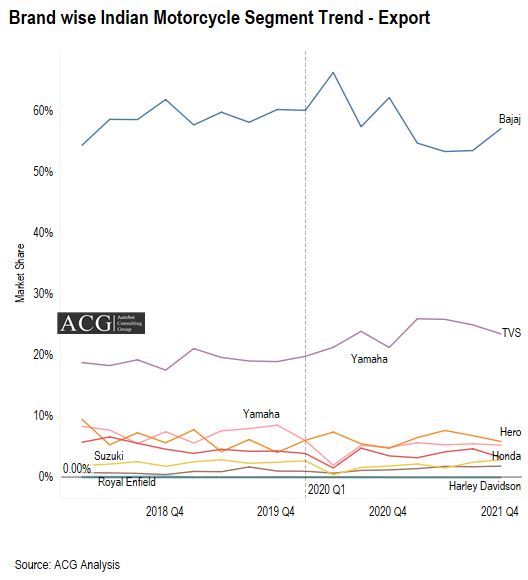

Indian Motorcycle Segment Trend: Export

Bajaj which used to perform decently well had to concede 20% of its existing market share during the last two years. But right after the 3rd quarter in 2021, Bajaj was back to business by conquering its lost share. Their fellow counterparts like Suzuki, Yamaha, and Hero were successful to an extent by being able to get that much-needed growth despite the adversities posed by the pandemic.

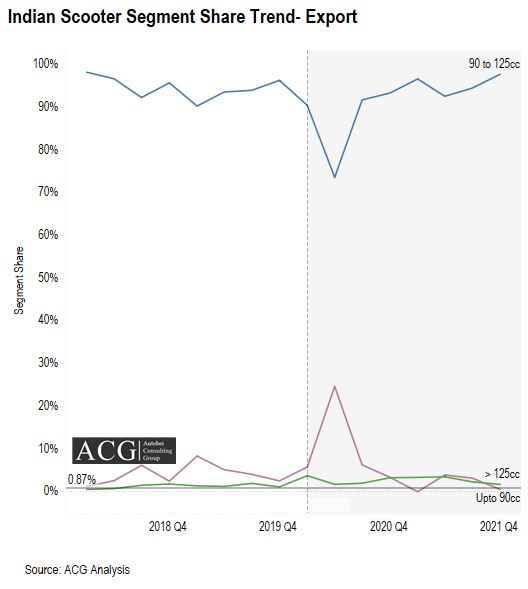

Indian Scooter Segment Trend: Export

The last two years of Pre Covid didn’t really give much of an opportunity for this particular market segment. 90 to 125cc showed attractive demand for the export market.

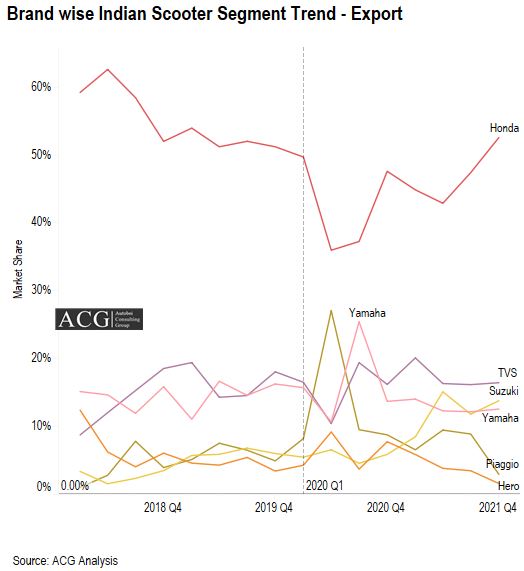

Honda is the market leader in the Scooter export segment. TVS is the second-largest player in scooter export.

To buy the full report, kindly contact at info@autobei.com