Electric Car Report Store is a one-stop solution for Electric Car start-ups, Entrepreneurs, Investors, OEMs, Suppliers, Market Research firms, SDV, and other service providers. ACG has key expertise in Electric car Products, Sales, Pricing, Entry Strategy, Customer Analytics, and Feasibility Studies of EVs and Components.

The Electric car package is a Master report package for OEMs, Venture Capital, Start-ups, Research firms, and Component suppliers. We prepared this package because it covers or touches every major business arm of the Electric car Business.

We created this exclusive Electric Car package so the client can get a 360-degree view of customer behaviour to the component-level supply chain value chain. The report bundle provides insight into how different EV verticals connect and how to use this information for EV business in Europe, India, and the USA.

The bundle report is affordable compared to buying individual EV reports. Purchasing a single package means making faster strategic decisions, as all EV market Intelligence is consolidated.

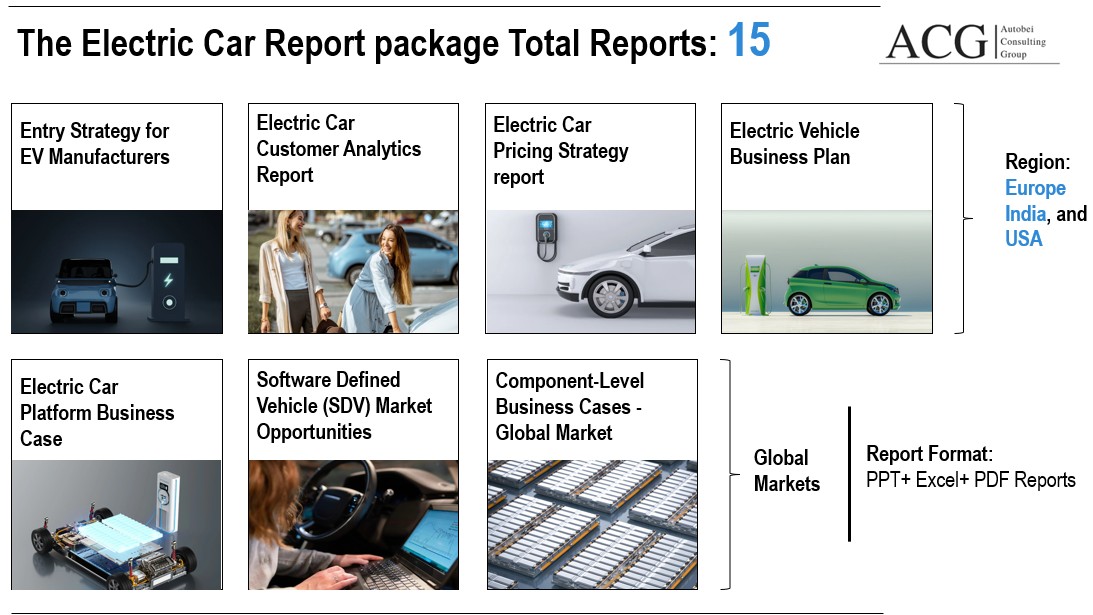

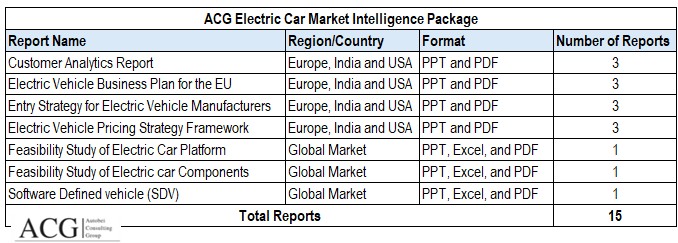

A total of 15 reports are available under this package:

In this package of Electric Car reports, we have covered the Demand side (Customer Analytics, Pricing Strategy, Business Plan) and the supply side, such as the EV component business case.

Our EV package also covers a 360-degree view of the Electric car supply and value chain from end user to OEM business strategy and drills down to EV ecosystem component supply.

The EU, the USA, and India are among the Key markets for Electric cars. We are offering key reports and a Feasibility Study in a single bundle:

The following are the reports available under this EV Package: Total Reports 15

Electric Car Market & Strategy

European Region Electric Car Report Package:

-

- Customer Analytics Report –

- Number of Pages: 60

- Format: PPT and PDF

- Electric Vehicle Business Plan for the EU

- Number of Pages: 60

- Format: PPT and PDF

- Entry Strategy for Electric Vehicle Manufacturers

- Number of Pages: 97

- Format: PPT and PDF

- Electric Vehicle Pricing Strategy Framework

- Number of Pages: 130

- Format: PPT and PDF

- Customer Analytics Report –

Indian Electric Car Report Package:

-

- Customer Analytics Report

- Number of Pages: 55

- Format: PPT and PDF

- Electric Vehicle Business Plan for India

- Number of Pages: 97

- Format: PPT and PDF

- Entry Strategy for Electric Vehicle Manufacturers

- Number of Pages: 110

- Format: PPT and PDF

- Electric Vehicle Pricing Strategy Framework

- Number of Pages: 95

- Format: PPT and PDF

- Customer Analytics Report

USA Electric Car Report Package:

-

- Customer Analytics Report

- Number of Pages: 51

- Format: PPT and PDF

- Electric Vehicle Business Plan for India

- Number of Pages: 106

- Format: PPT and PDF

- Entry Strategy for Electric Vehicle Manufacturers

- Number of Pages: 178

- Format: PPT and PDF

- Electric Vehicle Pricing Strategy Framework

- Number of Pages: 88

- Format: PPT and PDF

- Customer Analytics Report

Technology and Platform

Feasibility Study of Electric Car Platform:

-

- Number of Pages: 324

- Format: PPT, Excel, and PDF

Software Defined Vehicle (SDV) Opportunities:

-

- Number of Pages: 312

- Format: PPT, Excel, and PDF

Electric Car Component level Business cases

Feasibility Study of Electric car Components:

- Battery System

- Power Electronics

- Electric Motors

- Charging Systems

- Infotainment and Connectivity Systems

- Safety Systems and ADAS

- Thermal Management System

- Number of Pages: 178

- Format: PPT, Excel, and PDF

Various EV report advantage’s: USA, EU and India

- Customer analytics– Help Understand customer buying pattern, expectations, Preferences, and Price elasticity of the Electric Car in USA, EU, and India.

- Pricing and GTM Report: Roadmap for Entry Strategy, Positing, Product strategy, brand Strategy, Price point, Product portfolio, EV factory setup cost, and Revenue or ROI analysis

- EV Business Plan: Key document for investor, ROI, Forecast, and Blueprint for Electric car business in USA, EU, and India

- EV components Business case: Opportunities Analysis of supply chain ( Battery, Power Module, Motor)

- Electric car Platform Business case: About long term planning, Feasibility, Scaling, and R&D.

- Software defined vehicle (SDV): Opportunities and market demand analysis for Global SDV suppliers

Other advantages of Electric car package reports:

- ACG Electric car package or bundle reports provide ready made dossier for pitching to Venture capitals, Banks or Policy maker to take quick decision.

- Covered both commercial and technical aspects of the Electric car business.

- Mostly the individual reports does not align with other aspects like buying only pricing report does not align with the customer analytics, or Business plan.

Contact at info@autobei.com to get the detailed of the Table of Content of the each report

This is the most attractive price design for a specific application of short-distance distribution. The Tata ACE PRO payload is 750T, the LFP battery size is 14.4 kWh, and the real range is 130 km. Other Tata ACE EV products are the Tata Intra EV and Tata ACE EV 1000. The company is promoting heavily on digital platforms.

This is the most attractive price design for a specific application of short-distance distribution. The Tata ACE PRO payload is 750T, the LFP battery size is 14.4 kWh, and the real range is 130 km. Other Tata ACE EV products are the Tata Intra EV and Tata ACE EV 1000. The company is promoting heavily on digital platforms.