ACG released the latest report on Customer preference towards Electric Cars. The fast-paced world of today is the end result of many successful ideas that have been implemented with the right business strategy. If we consider any business model that has rendered fruitful results to the owner, then such a business will be governed by various factors, pivotal of them would be the consumer base and the specification in which it is offered viz. pricing, efficiency, uniqueness, etc. But the market dynamics slightly change in regards to the booming EV industry, and we need to bring in a completely different approach to ascertain its growth strategy. Any newness in the market will never be welcomed with an open arm, and the same goes with the EV industry as well. Similarly, even the EV segment faced a lot of problems in the initial phase, as the customers cited a lot of apprehension in regards to its efficiency, build, and other aspects.

Whenever a product is presented into the market, then the buyers look for the uniqueness coupled with affordability to own it, and the EV sector is still not able to present their product in the market with a cheaper tag nor an exorbitant mileage on offer, or vast reach of charging places. The research analysis that would be carried out as we deep dive into the core, will further unravel various factors that will influence the locomotion concerns. The following factors have proven to be the quintessential for deciding the success of EV: Option to get a feasible Charging point, an alternate mode of transport, especially cars to facilitate commuting, the cutting edge systems in place to boost the mileage efficiency.

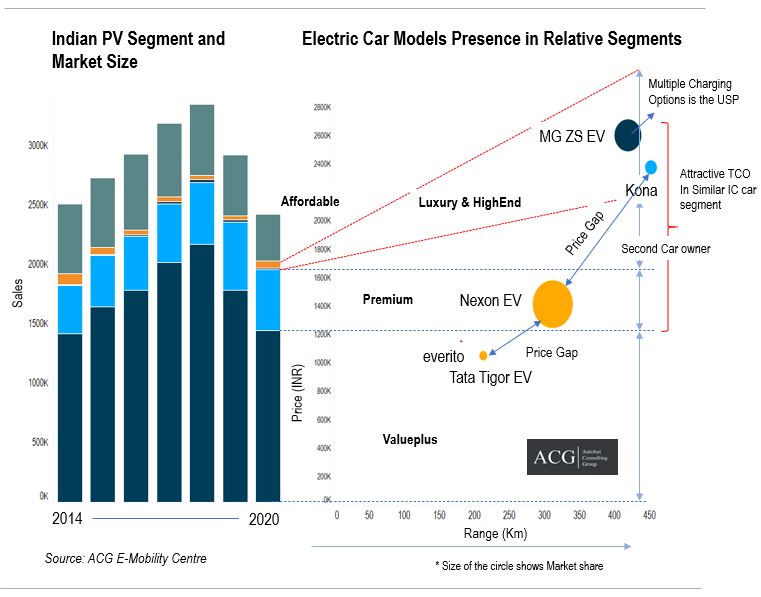

We have been able to ascertain that an ample kilometer coverage for an EV to be considered as good or worthy can stand starting from as low as 95km to a maximum reach of up to 260km.

The transition to the field of Electric Mobility has challenges of its own viz. inadequate charging infrastructure, shorter range, and time-consuming charging.

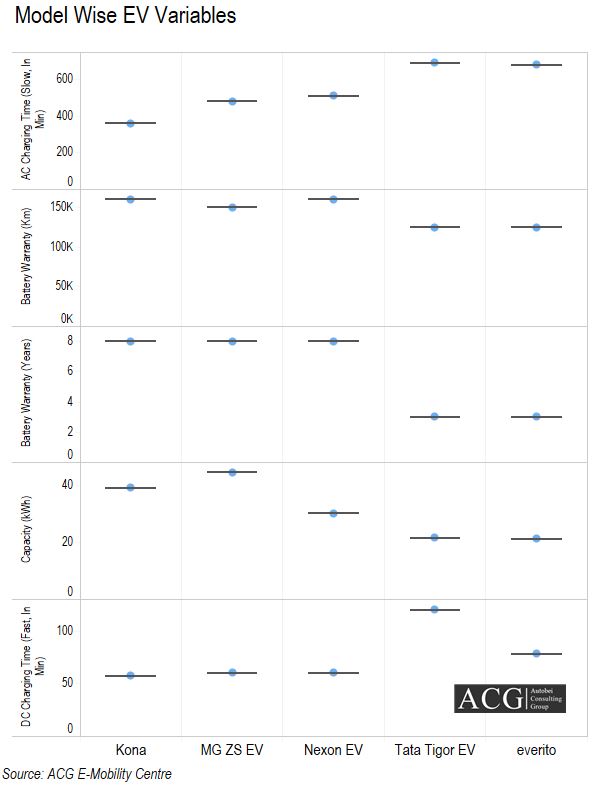

In the current market scenario Tata Nexon, MG EV Hector, Tata Tigor EV, Hyundai Kona are the Top products in the Market.

Electric Cars Product Performance:

After a keen inspection of the Locomotion structure, We can deduce the need of strengthening the fundamentals and the observation is as listed below:

Option to get a feasible charging point:

In the domain of EV, the energy fuelling stations have attained utmost importance and are indeed very integral for its operation. When we take a glance at Germany, France, the United Kingdom, and China market, which flaunts the topmost active users of the eco-friendly vehicle, it can be seen that the major amount of EV sales belongs to the region that has a vast amount of energy refueling stations.

An alternate mode of transport, especially cars to facilitate commuting:

The presence of commuting alternatives always reduces the risk associated with moving from one place to the other, and the inception of EVs has paved a way for the customers to prioritize EV’s as their next priority choice of vehicle or even as the primary. Luckily, this factor has turned out to be a blessing in disguise for the EV industry.

The end users anticipate a comprehensive system in place so that it can render practical solutions to all their locomotion needs. This aspect also seems to be the need of the hour, as many users may need to take up travel across the city or states owing to relatives function, various events, sightseeing, etc. As per the observations made from the recent analysis amassing a handful of commuters from various metropolitan cities concluded that there are instances where the drivers are supposed to drive greater than 1000 Kilometres and this sought of situation arises on a maximum of 30 to 40 days per year, as per the report. Since the EV has not yet been empowered to carry out trips on a stretch, this would continue to haunt the sprawling growth of EV and would be a major hurdle in the path of its adoption as the primary car of the users.

This structured article aims at exploring the three vital things influencing the commuting concerns on adoption to EV i.e Kind of energy refueling facility or point availability, the need of owning a second commuting option, lastly the mileage extent influencer system.

The EV’s available in the market is one of the commuting facilities that are available to access with certain characteristics, and these characteristics at times may not be feasible to meet one’s own needs or usage. What matters most to the drivers is the mileage efficiency, higher energy refueling times, and sparingly available charging points and these concerns need an efficient and immediate addressal so as to facilitate all their travel requirements.

The EV’s on the other hand find their space in the locomotion option, if in case an alternate car is available at any given point of time. Studies have also revealed certain points that the mobility issues seem to be very negligible with the users with an option of an additional car, and this can be any car that runs with conventional fuel.

The kind of trends that are seen amidst the community of owners who own multiple cars and then shift towards EV is: Initially, they try to fit in EV in the place of the user for shorter commuting needs, as the range that needs to be traversed falls under the purview of actual EV range, and the EV’s when harnessed for this need will perform to the expectation and nullify all the negative concerns. Apart from this, EV also tries to take it well past the user in the area of flexibility and thus boost the figures of EV in the arena of Universal travel distance. So, all these positives sum up to conclude the essentialness of EV and the need for it to evolve as a prime alternate commuting system though it does not find its use for everyday travel.

The cutting edge technologies in place to boost the mileage efficiency:

The topmost governing authority highlights that at times the Shorter mileage offered by EV’s acts as a thoughtful psychological barrier. When we analyze and comprehend the desirability of EV’s range then the user community is polarised to overestimate the total distance they need to cover, and underlines this more than their travel needs. Usually, these concerns are the end result of anticipating the risk of being prone to breakdown, running out of fuel or energy on the highways and in the vulnerable areas viz. forest, village roads, nomans place, etc. Also in case of an unplanned trip, these concerns will haunt even more as the driver needs to take up the commute without the knowledge of the kilometers to be covered, as they will not be aware of it beforehand. This will put them into a situation where they will not be able to furnish their travel needs owing to the miscalculation of the total distance to be covered and other factors. The study conducted taking into consideration 100 EV users of silicon city of India, revealed the stressful situations they face owing to the lesser mileage of EVs is arising in a recurrent fashion and poses a threat to the end-users at least 12 times a year.

Technology is the boon to the field of EV, and it is the need of the hour for the manufacturers to come up with an application that serves the purpose of giving end to end information about the EV car to the user, like What is the vehicle condition, Total mileage that can be achieved, Next service duration and lot more.

When it comes to the performance and capabilities of EV, we can say that it has undergone a swift change and its significance as well. But the evolving customer mindset has posed a great threat to it, and the failure of EV manufacturers in building a system to identify end users’ aspirations has blown the issue out of proportion.

The Manufacturing company-related aspects like the Value of the manufacturer and his position in the market, impeccable consumer facilitation, ability to retain the users play a very vital role in influencing customer’s mindsets and prove to be quintessential in their decision-making process of owning an EV.

Strategy for Building the product and the segment it can fall in:

The influential factors like Brand perception or social status tend to occupy the foremost importance when customers have the option of owning a Luxurious vehicle at the same cost as buying an entry-level trim of EV.

The EV buyers of the present world are in search of getting the best in class cutting edge features, they are versatile, passionate to own a car and they consider this owning affair to be a vibrant period. But ironically, the customers who value all the aforesaid points are not existing everywhere and their presence in the contemporary market almost tends to zero.

The prominent area of performance in the automotive sector is the lookout for superior vehicle acceleration by the customers. The best luxurious vehicles of today keenly encash on this aspect by advertising the time elapsed in seconds by their car to accelerate from 0 to a certain km range.

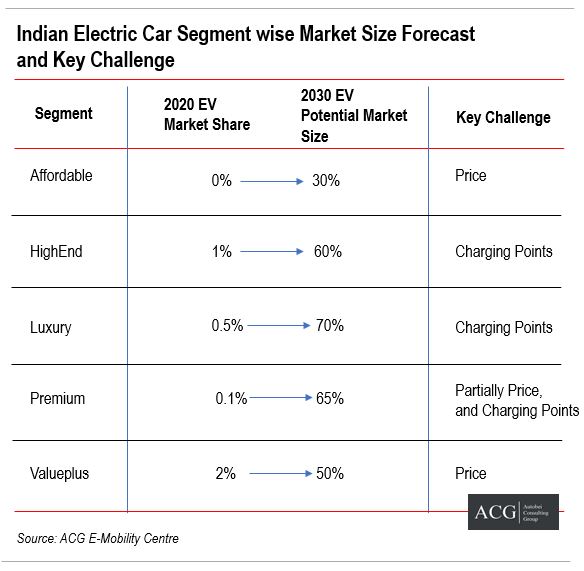

To conclude, we can clearly highlight the enormous amount of importance that is being rendered to the concept of Speed and Throttle maximize level. Categorically we can say that Cars that take the mentioned points into consideration will have a presence in the market of the following types: Affordable, Value Plus, Premium, Luxury, and Highend Cars.

To conclude, we can say the need for attention to detail cited by the customers is very much instrumental in amassing the sales figures and thereby contributing to the growth of the Product.

The world today is driven by technology, and technology has had an impeccable impact on our lifestyle too. These days owning a car is not only for commuting means but also reflects one’s own societal status. Despite the root cause of procuring a car is travel needs but it all boils down to the user’s perspective. There might be other influential factors for the owner to buy a car, such as updating the car to the one with larger capacity so as to accommodate additional members, passionate to get the taste of the advancement in the market that may, in turn, contribute for the higher efficiency and best in class feel. The above-listed features are pivotal in making the choice of the car.

So, Which according to you is the instrumental thing that will have its effect on the procurer to get a car for himself/herself? The Response for this will be ‘Procuring amount’.

Many of the customers have a restricted budget for procuring the vehicle. Cars are considered to be one of the fundamental purchases and the price one can afford to own is very restricted owing to a fixed cash flow. The EV’s are yet to get a level playing field and at times find it difficult to compete with the existing market, as the cost to own an EV is extremely high for a middle-class family and the high cost is due to the battery and its build architecture. The overall Amount that needs to be spent for buying an EV car is a very costly affair compared to owning a 4 wheeler with an ICE.

The scientific point that needs to be observed here is the slightly costlier investment in Electric vehicles, which can be largely reimbursed by saving considerable amounts in energy dissipation, service, and a lot more aspects. But it is very saddening, that the potential car procurer will pay the least attention to this broader concept. They consider that the savings they will be able to make is very inferior and assume to count it as fairly minimal than the product investment they make. As a product architect, one can perceive to get a thought of luring the customers by gradually scaling down the product cost by rendering govt aided funds or freeing them from tax, else the manufacturer can carry out impeccable research on the battery architecture, and thereby present an economical battery solution so as to address the high manufacturing cost and scale it down in the near future.

There also exists an idea proposed by Better Place, which seems to be practically feasible if efficiently implemented, like letting the customers purchase an electric-powered car with no battery. The customer in this case can be given an option of taking the electric fuel endowment or renting them on the basis of trips. This can be achieved by charging the customer only for distance covered, or a 7 day,30 days plan. This implementation can largely address the High-cost product issue.

Indeed, Better Place came up with a Superior sequel of this feature, which included a specific energy interchangeable infrastructure and also a closed-loop charging infrastructure. They claimed that the battery Interchanging process of replacing the charged battery with an already drained battery in the car can be done within a quarter of an hour, and this innovation is superior compared to the already existing fast charging services of today’s world. But, the hurdle in the path of achieving this mode of operation is that the concept of battery packet changing needs global acceptance and the same has not yet been acquired to date.

Things that are also equally impactful in owning a car are the specifications and the characteristics inculcated in the car, like the orientation of the structural part and vehicle trim. The vehicle trim choice is completely dependent on one’s own requirements and needs. For instance, a group of 7 people will aspire to strike a deal of owning an SUV or MPV kind of car than a 4 seater hatchback. As we take a glance at the existing electric models, interestingly we find a notable amount of impeccably enriched sedans and large SUVs.

Though many people were of the opinion that electric vehicles would storm the market as a hatchback, Tesla’s advent into the market presented a Sports racer and a Luxurious sedan. This was the precedent set by Tesla, and the other manufacturers in the lineup seemingly embraced the market with the same approach. This move of them is to be well appreciated. The strength of an electric sports car has always been its speed or the ability to needle up beyond the normal speed. The car savvy’s have time and again proved that they are all ready to procure the Investment for attaining higher speed. Yet another factor that is plaguing the slow-paced adoption of electric vehicles is its operationality.

The psychological thought which is prevalent in the world today is that the influence of the people around and their choices on an individual is immense: If your classmate, co-worker, people in the vicinity and acquaintance procure a number of EVs’s and in case they share a good review with you, then eventually your thought process bends towards making a similar choice.