Everyone asks the same two questions about electric trucks. Do they have enough range? And where will they charge? Our data says the answer is closer than you think. A small increase in electric truck range — sometimes just 3.3 km — opens new freight corridors for OEMs and fleet owners. We mapped 100-plus electric truck variants against India’s 24 priority freight corridors. The results change the range debate.

Take one example. The Ashok Leyland 14T BOSS sits just ~5 km short of the Delhi–Agra corridor. That gap needs no bigger battery. Software optimization, better semiconductors, or improved heat control can close it. A 19T BOSS range increase of about ~30 km would unlock Pune–Nashik as well — nine new corridors in total, each on a single charge.

One note on scope. The Mumbai–Delhi route is India’s busiest freight artery. We exclude it here because of its distance. It needs a separate charging analysis.

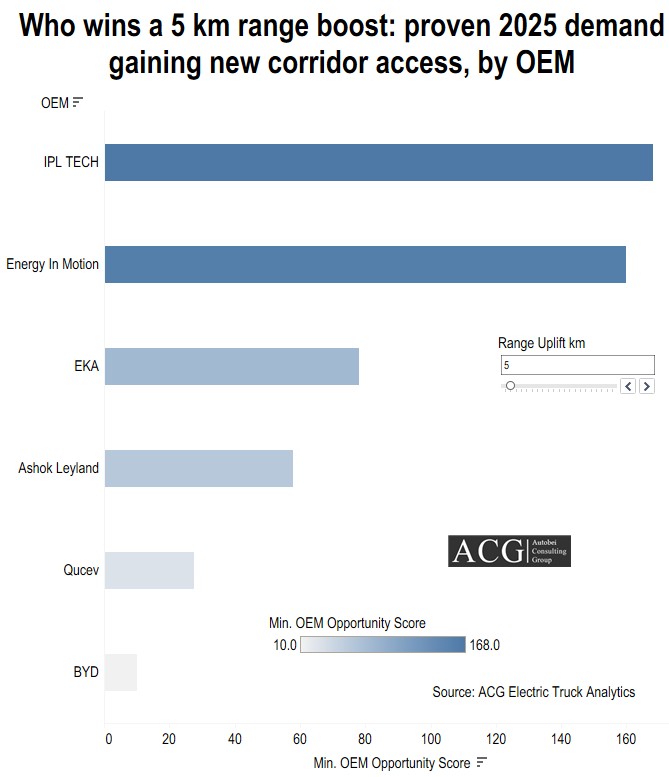

Which OEMs gain most from an electric truck range increase?

IPL Tech tops our opportunity scorecard with a score of 199. A minimal change in range could add more than 500 unit sales in a year. Energy in Motion (EiM), EKA, Ashok Leyland, and QCEV follow on the leaderboard.

The key point: these gains need no bigger battery. No higher price. A small improvement in electric truck range opens new highway routes with the products these OEMs already sell.

Why electric trucks are feasible now:

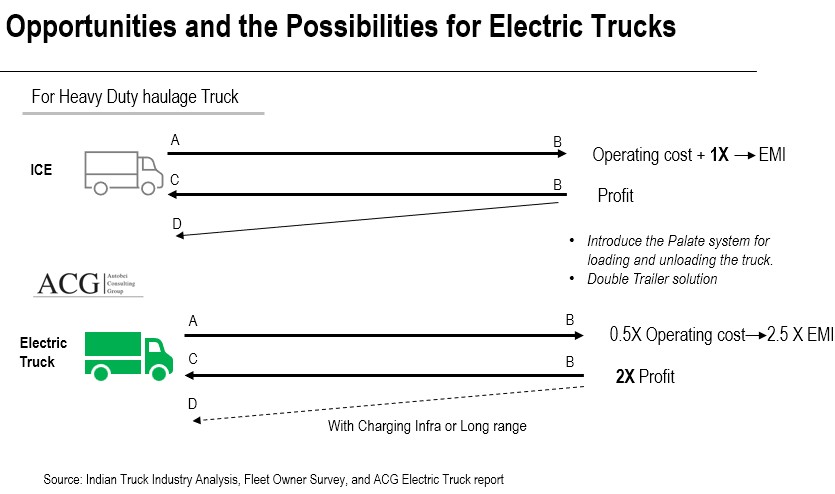

ICE and electric trucks operate on different economic models. Both work — under the right conditions.

Consider a heavy-duty, long-haul fleet owner. With a diesel truck, one-way freight revenue covers fuel, tolls, and expenses. The return trip is profit. Sometimes a single trip covers the monthly EMI.

An electric truck’s EMI is higher — roughly 2.5 times that of a diesel truck. But its operating cost is far lower. The diesel money you save effectively pays the EMI. A round trip still covers the full cost. The economics close; they just close differently. We help logistics companies develop profitable electric truck business models.

The electric truck sales opportunity on 24 corridors:

India’s 24 priority corridors hold most of the commercially addressable e-truck market. Today, e-truck use is limited to specific applications, routes, and duty cycles. But picking corridors is only half the answer. The other half is matching real trucks to real routes.

So we mapped every available electric truck model and variant. We compared their ranges against corridor distances and charging-point needs. Several routes are ready now. Dhanbad–Kolkata, Paradeep–Barbil, Vijayawada–Visakhapatnam, and Ahmedabad–Mundra combine strong freight loads with manageable distances.

Ahmedabad–Mundra clearly shows the pattern. Trucks from Ashok Leyland, EKA, EiM, and IPL Tech need just one charging stop on this corridor. Blue Energy’s current models need more than one.

Small electric truck range gains, big corridor unlocks:

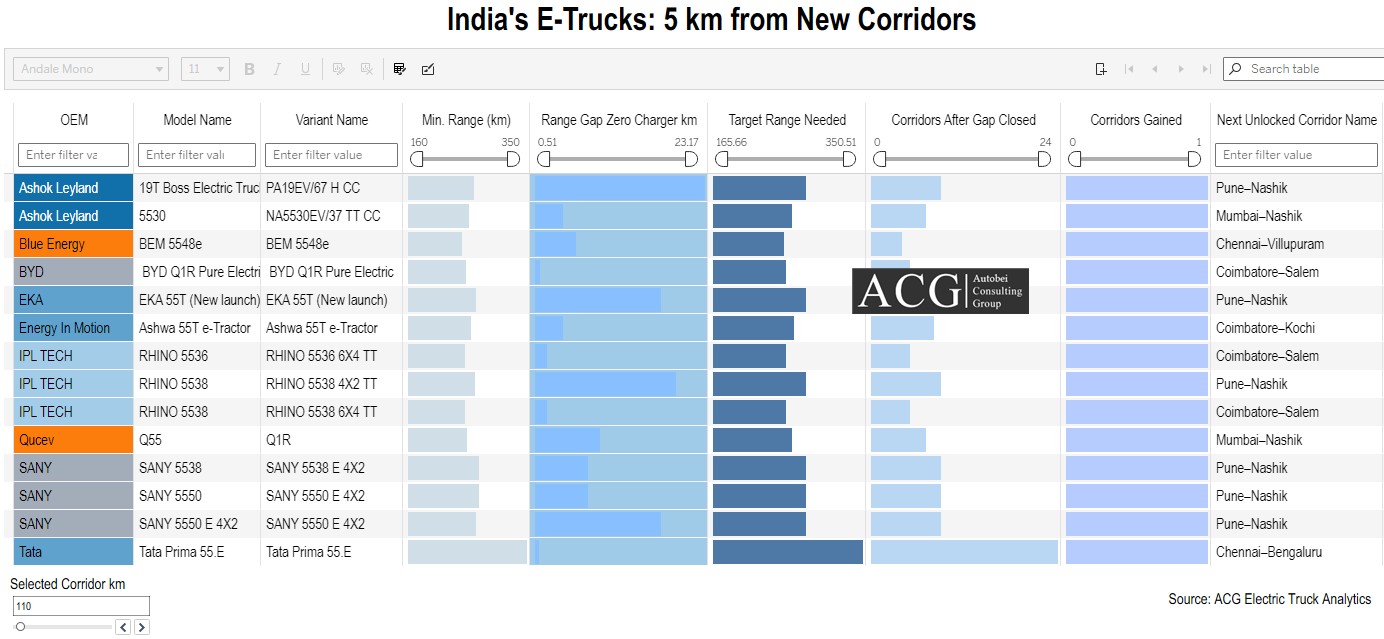

Our detailed report maps the exact range extension required for each variant to unlock each corridor. Two examples:

- The Ashwa 55E tractor needs about 4 km more range to unlock Coimbatore–Kochi.

- The BYD Q1R needs about 5 km more to unlock both the Ambala–Jalandhar and Coimbatore–Salem routes.

We ran this mapping for every model variant on every major route. The conclusion is consistent. Small range changes can lift an OEM’s electric truck sales by 30 to 40% in the near term.

Electric Truck Sales Forecast:

The PM E-DRIVE scheme targets 5,643 electric trucks in FY 2026. It offers ₹500 crore in demand incentives, with subsidies up to ₹9,60,000 per truck. Yet as of July 2026, only three trucks have claimed the incentive. The gap between policy and uptake is the market opportunity.

Our corridor math sizes it:

- Top 10 corridors: a market of about 600 trucks, led by high-profit routes.

- Top 24 corridors: about 2,500 trucks, with minimal new infrastructure.

- Top 50 corridors: up to 10,000 trucks by 2030 — if charging points expand and electric truck range keeps improving.

Truck type demand by corridor:

Different corridors demand different trucks and mix trucks. Delhi–Jaipur and Delhi–Chandigarh favor rigid haulage. FMCG and e-commerce drive the loads there.

What policymakers and logistics companies should do:

Start with one-stop corridors. Routes that need a single charging stop are the natural pilot projects. They are the fastest path to a proven green freight route.

Charging viability follows the trucks. Corridors already suited to electric trucks promise high charger utilization. That makes the business case for charging infrastructure companies.

Route certainty helps fleet owners. When charging stops are predictable, route planning risk drops. Confidence follows.

Pilots generate the data. Early operations will reveal real-world electric truck range by application. That data will optimize charging locations for everyone who comes next.

Inside the Full Report: 5 Strategic Insights That Can Give You a Competitive Advantage

- The complete unlock map — every one of the 100+ variants, matched to all 24 corridors, with the exact kilometers each needs to enter each new route. Which of your models is closest?

- The ranked opportunity scorecard — all OEM scores behind IPL Tech’s 199, weighted by real 2025 sales. See exactly where your brand stands and why.

- The one-stop corridor list — every route a truck can serve with a single charging stop today, ranked by freight load. The shortlist for pilots and charger siting.

- The round-trip economics model — how a 2.5× EMI still pays back per trip, corridor by corridor, with the diesel-equivalent math shown.

- Corridor-wise demand forecast to 2030 — the truck types, volumes, and infrastructure triggers behind the 600 / 2,500 / 10,000 truck scenarios.

RECOMMENDED REPORTS

The Future of Electric Trucking

June, 2026

Winning in the Indian Truck Market

June, 2026

Indian Bus Market and Product Analytics

June, 2026