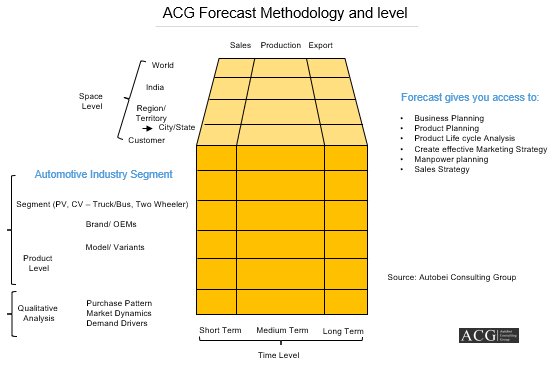

Every Year ACG released most detail and critical Research Report on Indian Automobile Industry Report which covers all major vertical of Industry including Electric Vehicle and Govt policies to promote it. The report contains Historical Trend and next 5 years forecast. Indian is expected to be among the Globally top 3 markets by 2030 by touching USD 270 billion. We analyzed multiple factors which influenced the Automotive sector. This also helps the foreign and Indian companies which are planning to invest in the Automobile sector. The report is available on subscription-based also. The Monthly and Quarterly subscription option is available to get every pulse of the industry movement.

Each chapter gives qualitative analysis, Challenges, Opportunities, and Market Drivers also. Additional information like Doing business in India, Finding a partner in India, Consumer buying behavior, Product launching strategy, Marketing & Branding Strategy, Digital solution, Sales Planning, and Business etiquette in India.

Table of Content of the report:

1 Summary

2 Automobile Industry Overview

3 Methodology and Limitation of Study

4 Country Analysis – India

4.1. Politics

4.2. Economy

4.3. Risk

4.4. Regulation

4.5. Business

4.6. Industry

4.7. Culture

5. Auto Industry Statistics Analysis – Since 2013 to 2017

6. Indian Automotive Industry Overview and Segment Analysis

7. Passenger Vehicle

7.1. Car

7.1.1. Market Size (Unit & Value)

7.1.2. Segment Share

7.1.3. Growth

7.1.4. Latest updates

7.1.5. New Product Launched

7.2. UV/SUV

7.2.1. Market Size (Unit & Value)

7.2.2. Segment Share

7.2.3. Growth

7.2.4. Latest updates

7.2.5. New Product Launched

7.3. Van

7.3.1. Market Size (Unit & Value)

7.3.2. Segment Share

7.3.3. Growth

7.3.4. Latest updates

7.3.5. New Product Launched

8. Commercial Vehicle

8.1. Medium & Heavy Commercial Vehicle

8.1.1. Market Size (Unit & Value)

8.1.2. Segment Share

8.1.3. Growth

8.1.4. Latest updates

8.1.5. New Product Launched

8.2. Light Commercial vehicle

8.2.1. Market Size (Unit & Value)

8.2.2. Segment Share

8.2.3. Growth

8.2.4. Latest updates

8.2.5. New Product Launched

9. Two-Wheeler Analysis

9.1. Market Size (Unit & Value)

9.2. Segment Share

9.3. Growth

9.4. Latest updates

9.5. New Product Launched

10. Scooter (Unit & Value)

10.1. Sales Volume

10.2. Segment Share

10.3. Growth

11. Motorcycle (Unit & Value)

11.1. Sales Volume

11.2. Segment Share

11.3. Growth

12. Moped (Unit & Value)

12.1. Sales Volume

12.2. Segment Share

12.3. Growth

13. Three-Wheeler

13.1. Market Size (Unit & Value)

13.2. Segment Share

13.3. Growth

14. Three-Wheeler Passenger Vehicle

14.1. Sales Trend Analysis

14.2. Segment Share

14.3. Growth Analysis

14.4. Segment Share

15. Three-Wheeler Cargo Vehicle

15.1. Sales Trend Analysis

15.2. Production Trend Analysis

15.3. Export Trend Analysis

15.4. Segment Share

16. Passenger Vehicle Detail Analysis – Market Trend, Market Share and Growth

16.1. Market Size (Unit & Value)

16.2. Segment Share

16.3. Growth

16.4. Latest updates

16.5. New Product Launched

16.6. OEMs Sales, Market Share, and Growth Analysis

16.6.1. FIAT

16.6.1.1. Company Overview

16.6.1.2. Sales Volume

16.6.1.3. Market Share movement

16.6.1.4. Product Portfolio and Analysis

16.6.1.5. Production plant

16.6.2. Force Motors

16.6.2.1. Company Overview

16.6.2.2. Sales Volume

16.6.2.3. Market Share movement

16.6.2.4. Product Portfolio and Analysis

16.6.2.5. Production plant

16.6.3. Ford India

16.6.3.1. Company Overview

16.6.3.2. Sales Volume

16.6.3.3. Market Share movement

16.6.3.4. Product Portfolio and Analysis

16.6.3.5. Production plant

16.6.4. Hindustan Motor Fin. Corp.Ltd/Hindustan Motors Ltd

16.6.4.1. Company Overview

16.6.4.2. Sales Volume

16.6.4.3. Market Share movement

16.6.4.4. Product Portfolio and Analysis

16.6.4.5. Production plant

16.6.5. Honda

16.6.5.1. Company Overview

16.6.5.2. Sales Volume

16.6.5.3. Market Share movement

16.6.5.4. Product Portfolio and Analysis

16.6.5.5. Production plant

16.6.6. Hyundai

16.6.6.1. Company Overview

16.6.6.2. Sales Volume

16.6.6.3. Market Share movement

16.6.6.4. Product Portfolio and Analysis

16.6.6.5. Production plant

16.6.7. Isuzu Motors

16.6.7.1. Company Overview

16.6.7.2. Sales Volume

16.6.7.3. Market Share movement

16.6.7.4. Product Portfolio and Analysis

16.6.7.5. Production plant

16.6.8. Mahindra & Mahindra

16.6.8.1. Company Overview

16.6.8.2. Sales Volume

16.6.8.3. Market Share movement

16.6.8.4. Product Portfolio and Analysis

16.6.8.5. Production plant

16.6.9. Maruti Suzuki

16.6.9.1. Company Overview

16.6.9.2. Sales Volume

16.6.9.3. Market Share movement

16.6.9.4. Product Portfolio and Analysis

16.6.9.5. Production plant

16.6.10. Nissan Motor

16.6.10.1. Company Overview

16.6.10.2. Sales Volume

16.6.10.3. Market Share movement

16.6.10.4. Product Portfolio and Analysis

16.6.10.5. Production plant

16.6.11. Renault

16.6.11.1. Company Overview

16.6.11.2. Sales Volume

16.6.11.3. Market Share movement

16.6.11.4. Product Portfolio and Analysis

16.6.11.5. Production plant

16.6.12. Skoda

16.6.12.1. Company Overview

16.6.12.2. Sales Volume

16.6.12.3. Market Share movement

16.6.12.4. Product Portfolio and Analysis

16.6.12.5. Production plant

16.6.13. Tata Motor

16.6.13.1. Company Overview

16.6.13.2. Sales Volume

16.6.13.3. Market Share movement

16.6.13.4. Product Portfolio and Analysis

16.6.13.5. Production plant

16.6.14. Toyota

16.6.14.1. Company Overview

16.6.14.2. Sales Volume

16.6.14.3. Market Share movement

16.6.14.4. Product Portfolio and Analysis

16.6.14.5. Production plant

16.6.15. Volkswagen

16.6.15.1. Company Overview

16.6.15.2. Sales Volume

16.6.15.3. Market Share movement

16.6.15.4. Product Portfolio and Analysis

16.6.15.5. Production plant

16.6.16. Others

17. Commercial Vehicle Analysis

17.1. Total Indian CV Industry Market size – 2012 to 2017 (Unit & Value)

17.2. CV Market Share Analysis in Indian Automobile Industry

17.3. Sales Statistics

17.4. Production Statistics

17.5. Export Statistics

17.6. Growth Analysis

17.7. Key Market Drivers

18. Segment Analysis

18.1. Indian Commercial Vehicles: Market Classification

18.2. OEM Strategy Analysis

18.2.1. AMW Motors (Not in Operation)

18.2.1.1. Company Overview

18.2.1.2. Sales Volume

18.2.1.3. Market Share movement

18.2.1.4. Product Portfolio and Analysis

18.2.1.5. Production plant

18.2.2. Ashok Leyland

18.2.2.1. Company Overview

18.2.2.2. Sales Volume

18.2.2.3. Market Share movement

18.2.2.4. Product Portfolio and Analysis

18.2.2.5. Production plant

18.2.3. Force Motors

18.2.3.1. Company Overview

18.2.3.2. Sales Volume

18.2.3.3. Market Share movement

18.2.3.4. Product Portfolio and Analysis

18.2.3.5. Production plant

18.2.4. Isuzu Motors

18.2.4.1. Company Overview

18.2.4.2. Sales Volume

18.2.4.3. Market Share movement

18.2.4.4. Product Portfolio and Analysis

18.2.4.5. Production plant

18.2.5. Mahindra

18.2.5.1. Company Overview

18.2.5.2. Sales Volume

18.2.5.3. Market Share movement

18.2.5.4. Product Portfolio and Analysis

18.2.5.5. Production plant

18.2.6. Maruti Suzuki

18.2.6.1. Company Overview

18.2.6.2. Sales Volume

18.2.6.3. Market Share movement

18.2.6.4. Product Portfolio and Analysis

18.2.6.5. Production plant

18.2.7. Piaggio Vehicles Pvt Ltd

18.2.7.1. Company Overview

18.2.7.2. Sales Volume

18.2.7.3. Market Share movement

18.2.7.4. Product Portfolio and Analysis

18.2.7.5. Production plant

18.2.8. SML Isuzu Ltd

18.2.8.1. Company Overview

18.2.8.2. Sales Volume

18.2.8.3. Market Share movement

18.2.8.4. Product Portfolio and Analysis

18.2.8.5. Production plant

18.2.9. Tata Motors Ltd

18.2.9.1. Company Overview

18.2.9.2. Sales Volume

18.2.9.3. Market Share movement

18.2.9.4. Product Portfolio and Analysis

18.2.9.5. Production plant

18.2.10. VECVs – Eicher

18.2.10.1. Company Overview

18.2.10.2. Sales Volume

18.2.10.3. Market Share movement

18.2.10.4. Product Portfolio and Analysis

18.2.10.5. Production plant

18.2.11. VECVs – Volvo

18.2.11.1. Company Overview

18.2.11.2. Sales Volume

18.2.11.3. Market Share movement

18.2.11.4. Product Portfolio and Analysis

18.2.11.5. Production plant

18.3. Medium & Heavy Commercial Vehicle Analysis

18.3.1. Market Size and Trend Analysis

18.3.2. Segment and Market Share Analysis

18.3.3. Growth Analysis

18.3.4. Key players

18.3.5. OEMs Strategy Analysis

18.3.6. Tata Motors

18.3.6.1. Company Overview

18.3.6.2. Sales Volume

18.3.6.3. Market Share movement

18.3.6.4. Product Portfolio and Analysis

18.3.7. AMW (Not in Operation)

18.3.7.1. Company Overview

18.3.7.2. Sales Volume

18.3.7.3. Market Share movement

18.3.7.4. Product Portfolio and Analysis

18.3.8. VECV – Eicher

18.3.8.1. Company Overview

18.3.8.2. Sales Volume

18.3.8.3. Market Share movement

18.3.8.4. Product Portfolio and Analysis

18.3.9. VECV – Volvo

18.3.9.1. Company Overview

18.3.9.2. Sales Volume

18.3.9.3. Market Share movement

18.3.9.4. Product Portfolio and Analysis

18.3.10. SML Isuzu

18.3.10.1. Company Overview

18.3.10.2. Sales Volume

18.3.10.3. Market Share movement

18.3.10.4. Product Portfolio and Analysis

18.3.11. Daimler Indian Commercial Vehicle (BharatBenz)

18.3.11.1. Company Overview

18.3.11.2. Sales Volume

18.3.11.3. Market Share movement

18.3.11.4. Product Portfolio and Analysis

18.3.12. Scania Indian Commercial Vehicle

18.3.12.1. Company Overview

18.3.12.2. Sales Volume

18.3.12.3. Market Share movement

18.3.12.4. Product Portfolio and Analysis

18.3.13. MAN Trucks India (Closed its domestic Operation)

18.3.13.1. Company Overview

18.3.13.2. Sales Volume

18.3.13.3. Market Share movement

18.3.13.4. Product Portfolio and Analysis

18.4. Light Commercial Vehicle Analysis

18.4.1. Market Size and Trend Analysis

18.4.2. Segment and Market Share Analysis

18.4.3. Growth Analysis

18.4.4. Key players

18.4.5. OEMs Strategy Analysis

18.4.6. Tata Motors

18.4.6.1. Company Overview

18.4.6.2. Sales Volume

18.4.6.3. Market Share movement

18.4.6.4. Product Portfolio and Analysis

18.4.7. Ashok Leyland

18.4.7.1. Company Overview

18.4.7.2. Sales, Production and Export Statistics

18.4.7.3. Market Share movement

18.4.7.4. Product Portfolio and Analysis

18.4.8. Piaggio Vehicle

18.4.8.1. Company Overview

18.4.8.2. Sales, Production and Export Statistics

18.4.8.3. Market Share movement

18.4.8.4. Product Portfolio and Analysis

18.4.9. VECV – Eicher

18.4.9.1. Company Overview

18.4.9.2. Sales, Production and Export Statistics

18.4.9.3. Market Share movement

18.4.9.4. Product Portfolio and Analysis

18.4.10. Force Motors

18.4.10.1. Company Overview

18.4.10.2. Sales, Production and Export Statistics

18.4.10.3. Market Share movement

18.4.10.4. Product Portfolio and Analysis

18.4.11. Isuzu

18.4.11.1. Company Overview

18.4.11.2. Sales, Production and Export Statistics

18.4.11.3. Market Share movement

18.4.11.4. Product Portfolio and Analysis

18.4.12. Maruti Suzuki

18.4.12.1. Company Overview

18.4.12.2. Sales, Production and Export Statistics

18.4.12.3. Market Share movement

18.4.12.4. Product Portfolio and Analysis

18.4.13. Daimler Indian Commercial Vehicle (BharatBenz)

18.4.13.1. Company Overview

18.4.13.2. Sales, Production and Export Statistics

18.4.13.3. Market Share movement

18.4.13.4. Product Portfolio and Analysis

19. Two-Wheeler Industry Analysis

19.1. Statistics and Qualitative Analysis

19.1.1. Two-Wheeler Industry Volume Production

19.1.2. Two-Wheeler Industry Volume Sales

19.1.3. Two-Wheeler Industry Volume Export

19.1.4. Market Share in Indian Automobile Industry

19.1.5. Growth Analysis

19.1.6. Key Market Driver

19.1.7. Electric Two-Wheeler Overview

19.2. OEM Strategy Analysis

19.2.1. Bajaj Auto

19.2.1.1. Company Overview

19.2.1.2. Sales Volume

19.2.1.3. Segment presence and Analysis

19.2.1.4. Market Share movement

19.2.1.5. Product Portfolio and Analysis

19.2.2. Harley Davidson

19.2.2.1. Company Overview

19.2.2.2. Sales Volume

19.2.2.3. Market Share movement

19.2.2.4. Product Portfolio and Analysis

19.2.3. Hero MotoCorp

19.2.3.1. Company Overview

19.2.3.2. Sales Volume

19.2.3.3. Market Share movement

19.2.3.4. Product Portfolio and Analysis

19.2.4. Honda Motorcycle & Scooter

19.2.4.1. Company Overview

19.2.4.2. Sales Volume

19.2.4.3. Market Share movement

19.2.4.4. Product Portfolio and Analysis

19.2.5. India Kawasaki Motors

19.2.5.1. Company Overview

19.2.5.2. Sales Volume

19.2.5.3. Market Share movement

19.2.5.4. Product Portfolio and Analysis

19.2.6. India Yamaha Motor

19.2.6.1. Company Overview

19.2.6.2. Sales Volume

19.2.6.3. Market Share movement

19.2.6.4. Product Portfolio and Analysis

19.2.7. Mahindra Two Wheelers

19.2.7.1. Company Overview

19.2.7.2. Sales Volume

19.2.7.3. Market Share movement

19.2.7.4. Product Portfolio and Analysis

19.2.8. Piaggio Vehicles

19.2.8.1. Company Overview

19.2.8.2. Sales Volume

19.2.8.3. Market Share movement

19.2.8.4. Product Portfolio and Analysis

19.2.9. Royal Enfield (Unit of Eicher Ltd)

19.2.9.1. Company Overview

19.2.9.2. Sales Volume

19.2.9.3. Market Share movement

19.2.9.4. Product Portfolio and Analysis

19.2.10. Suzuki Motorcycle

19.2.10.1. Company Overview

19.2.10.2. Sales Volume

19.2.10.3. Market Share movement

19.2.10.4. Product Portfolio and Analysis

19.2.11. Triumph Motorcycles

19.2.11.1. Company Overview

19.2.11.2. Sales Volume

19.2.11.3. Market Share movement

19.2.11.4. Product Portfolio and Analysis

19.2.12. TVS Motor Company

19.2.12.1. Company Overview

19.2.12.2. Sales Volume

19.2.12.3. Market Share movement

19.2.12.4. Product Portfolio and Analysis

19.3. Motorcycle Industry Analysis

19.3.1. Motorcycle Industry Sales Volume

19.3.2. Market Share in Indian Automobile Industry

19.3.3. Growth Analysis

19.3.4. Key Market Driver

19.3.5. Motorcycle OEM Market Analysis

19.3.5.1. Bajaj Auto

19.3.5.1.1. Sales Volume

19.3.5.1.2. Market Share movement

19.3.5.1.3. Product Portfolio and Analysis

19.3.5.2. Harley Davidson

19.3.5.2.1. Sales Volume

19.3.5.2.2. Market Share movement

19.3.5.2.3. Product Portfolio and Analysis

19.3.5.3. Hero MotoCorp

19.3.5.3.1. Sales Volume

19.3.5.3.2. Market Share movement

19.3.5.3.3. Product Portfolio and Analysis

19.3.5.4. Honda Motorcycle & Scooter

19.3.5.4.1. Sales Volume

19.3.5.4.2. Market Share movement

19.3.5.4.3. Product Portfolio and Analysis

19.3.5.5. India Kawasaki Motors

19.3.5.5.1. Sales Volume

19.3.5.5.2. Market Share movement

19.3.5.5.3. Product Portfolio and Analysis

19.3.5.6. India Yamaha Motor

19.3.5.6.1. Sales Volume

19.3.5.6.2. Market Share movement

19.3.5.6.3. Product Portfolio and Analysis

19.3.5.7. Mahindra Two Wheelers

19.3.5.7.1. Sales Volume

19.3.5.7.2. Market Share movement

19.3.5.7.3. Product Portfolio and Analysis

19.3.5.8. Royal Enfield (Unit of Eicher Ltd)

19.3.5.8.1. Sales Volume

19.3.5.8.2. Market Share movement

19.3.5.8.3. Product Portfolio and Analysis

19.3.5.9. Suzuki Motorcycle

19.3.5.9.1. Sales Volume

19.3.5.9.2. Market Share movement

19.3.5.9.3. Product Portfolio and Analysis

19.3.5.10. Triumph Motorcycles

19.3.5.10.1. Sales Volume

19.3.5.10.2. Market Share movement

19.3.5.10.3. Product Portfolio and Analysis

19.3.5.11. TVS Motor Company Ltd

19.3.5.11.1. Sales Volume

19.3.5.11.2. Market Share movement

19.3.5.11.3. Product Portfolio and Analysis

19.4. Scooter OEM Market Analysis

19.4.1. Scooter Industry Market Size

19.4.2. Market Share in Indian Automobile Industry

19.4.3. Growth Analysis

19.4.4. Key Market Driver

19.4.5. OEM Strategy Analysis

19.4.5.1. Piaggio

19.4.5.1.1. Sales Volume

19.4.5.1.2. Market Share movement

19.4.5.1.3. Product Portfolio and Analysis

19.4.5.2. Hero MotoCorp

19.4.5.2.1. Sales Volume

19.4.5.2.2. Market Share movement

19.4.5.2.3. Product Portfolio and Analysis

19.4.5.3. Honda Motorcycle & Scooter

19.4.5.3.1. Sales Volume

19.4.5.3.2. Market Share movement

19.4.5.3.3. Product Portfolio and Analysis

19.4.5.4. India Yamaha Motor

19.4.5.4.1. Sales Volume

19.4.5.4.2. Market Share movement

19.4.5.4.3. Product Portfolio and Analysis

19.4.5.5. Mahindra Two Wheelers

19.4.5.5.1. Sales Volume

19.4.5.5.2. Market Share movement

19.4.5.5.3. Product Portfolio and Analysis

19.4.5.6. Suzuki Motorcycle

19.4.5.6.1. Sales Volume

19.4.5.6.2. Market Share movement

19.4.5.6.3. Product Portfolio and Analysis

19.4.5.7. TVS Motor Company Ltd

19.4.5.7.1. Sales Volume

19.4.5.7.2. Market Share movement

19.4.5.7.3. Product Portfolio and Analysis

20. Indian Three-Wheeler Industry Analysis

20.1. Statistics and Qualitative Analysis

20.1.1. Three-Wheeler Industry Market size

20.1.2. Market Share in Indian Automobile Industry

20.1.3. Key Drivers

20.1.4. Growth Analysis

20.1.5. OEM Strategy Analysis

20.1.5.1. Bajaj Auto

20.1.5.1.1. Sales Volume

20.1.5.1.2. Market Share movement

20.1.5.1.3. Product Portfolio and Analysis

20.1.5.2. Piaggio Vehicles

20.1.5.2.1. Sales Volume

20.1.5.2.2. Market Share movement

20.1.5.2.3. Product Portfolio and Analysis

20.1.5.3. TVS Motor

20.1.5.3.1. Sales Volume

20.1.5.3.2. Market Share movement

20.1.5.3.3. Product Portfolio and Analysis

20.1.5.4. Mahindra

20.1.5.4.1. Sales Volume

20.1.5.4.2. Market Share movement

20.1.5.4.3. Product Portfolio and Analysis

20.1.5.5. Atul Auto

20.1.5.5.1. Sales Volume

20.1.5.5.2. Market Share movement

20.1.5.5.3. Product Portfolio and Analysis

20.1.5.6. Piaggio Vehicles

20.1.5.6.1. Sales Volume

20.1.5.6.2. Market Share movement

20.1.5.6.3. Product Portfolio and Analysis

20.1.5.7. Scooters India

20.1.5.7.1. Sales Volume

20.1.5.7.2. Market Share movement

20.1.5.7.3. Product Portfolio and Analysis

20.2. Three-Wheeler Passenger Vehicle Analysis

20.2.1. Three-Wheeler Passenger Vehicle Volume Sales

20.2.2. Market Share in Indian Three-Wheeler Industry

20.2.3. Growth Analysis

20.2.4. Key Market Driver

20.2.5. OEMs Strategy Analysis

20.2.5.1. Bajaj Auto

20.2.5.1.1. Sales Volume

20.2.5.1.2. Market Share movement

20.2.5.1.3. Product Portfolio and Analysis

20.2.5.2. Atul Auto

20.2.5.2.1. Sales Volume

20.2.5.2.2. Market Share movement

20.2.5.2.3. Product Portfolio and Analysis

20.2.5.3. Mahindra & Mahindra

20.2.5.3.1. Sales Volume

20.2.5.3.2. Market Share movement

20.2.5.3.3. Product Portfolio and Analysis

20.2.5.4. Scooters India

20.2.5.4.1. Sales Volume

20.2.5.4.2. Market Share movement

20.2.5.4.3. Product Portfolio and Analysis

20.2.5.5. TVS Motor

20.2.5.5.1. Sales Volume

20.2.5.5.2. Market Share movement

20.2.5.5.3. Product Portfolio and Analysis

20.3. Three-Wheeler Cargo Carrier Analysis

20.3.1. Three-Wheeler Goods Carrier Volume Sales

20.3.2. Market Share in Indian Three-Wheeler Industry

20.3.3. Growth Analysis

20.3.4. Key Market Driver

20.3.5. OEM Strategy Analysis

20.3.5.1. Bajaj Auto

20.3.5.1.1. Sales Volume

20.3.5.1.2. Market Share movement

20.3.5.1.3. Product Portfolio and Analysis

20.3.5.2. Atul Auto

20.3.5.2.1. Sales Volume

20.3.5.2.2. Market Share movement

20.3.5.2.3. Product Portfolio and Analysis

20.3.5.3. Mahindra & Mahindra

20.3.5.3.1. Sales Volume

20.3.5.3.2. Market Share movement

20.3.5.3.3. Product Portfolio and Analysis

20.3.5.4. Scooters India

20.3.5.4.1. Sales Volume

20.3.5.4.2. Market Share movement

20.3.5.4.3. Product Portfolio and Analysis

20.3.5.5. TVS Motor

20.3.5.5.1. Sales Volume

20.3.5.5.2. Market Share movement

20.3.5.5.3. Product Portfolio and Analysis

21. Conclusion