The Indian Truck Industry showed 13% growth in FY 2026 compared to FY 2025. Due to demand in Construction and Mining applications, Tipper registered 11.7% growth. There was increased demand in E-commerce, Agricultural Products, and FMCG. The largest Tipper segments are 6X4 and 8X4 axle configurations with engine power above 200hp.

The Rigid Haulage showed 14.2% growth. Due to demand for 55T in applications such as steel and cement, the Tractor Trailer closed FY 2026 with single-digit growth compared to FY 2025. 10X2 and 6X2 are the largest segments within Rigid Haulage due to their favorable TCO and payback periods.

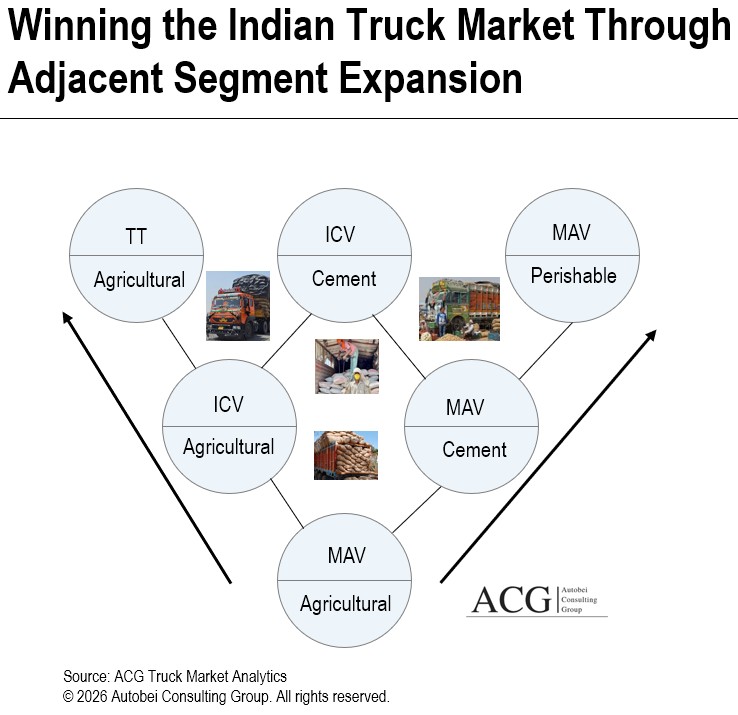

Application is the key and backbone of the Truck Industry. The next most important dimension is the segment. If the Suppliers or truck OEMs can find a closely aligned segment that can fit multiple truck segments, and vice versa.

Light-duty trucks and medium-duty trucks were in demand as drivers began to own their own trucks, single-driver driven, Lower toll, easy to get a load, and became single-fleet owners, and demand increased in regional transportation.

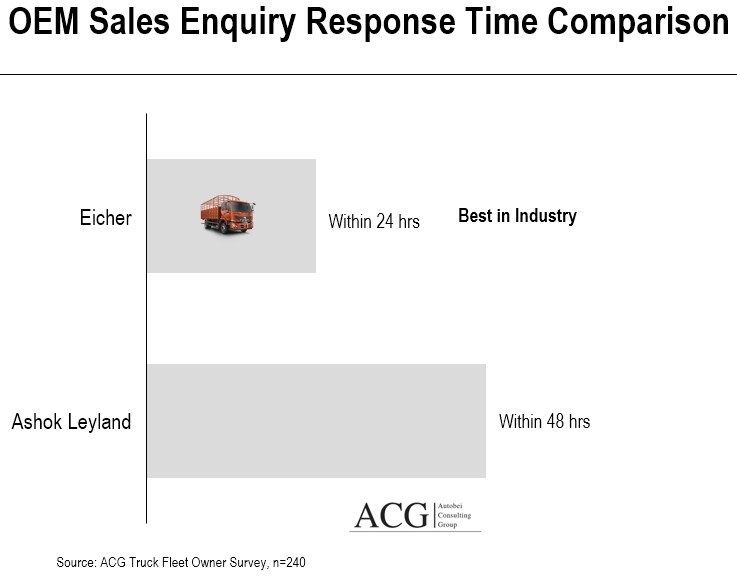

The Operating costs are low in the LDT and MDT truck segments. Models like the Eicher PRO 2110 are popular among Small and single-fleet owners. Eicher, Mahindra, and Ashok Leyland are the key leaders in this segment because their product ranges meet market requirements.

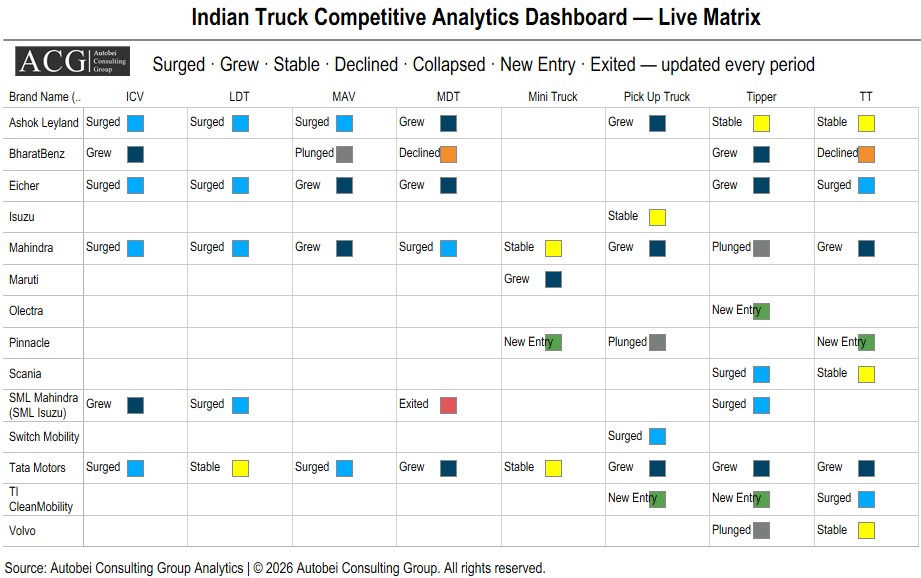

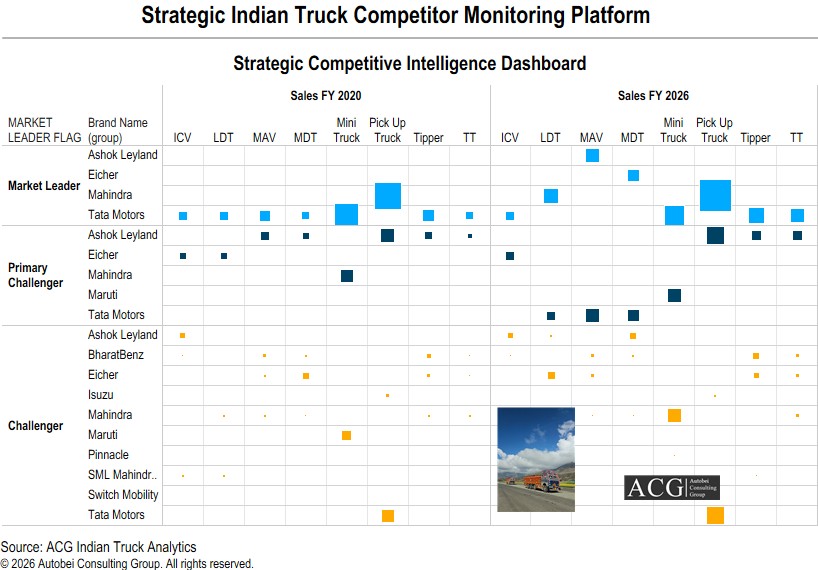

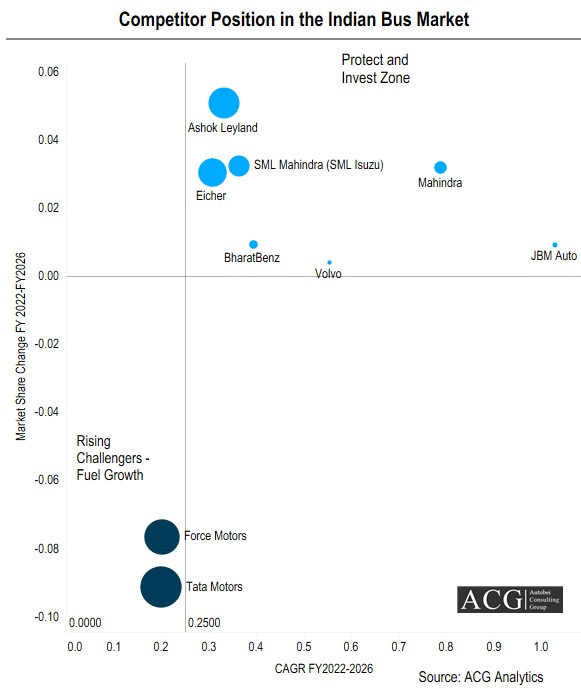

Indian Truck Competitor Position:

There are significant changes in the segmental leadership position of Tata Motors in FY 2026 compared to FY 2020 because new truck models were launched by Mahindra, Ashok Leyland, and Eicher.

We have developed a live Strategic Competitive Intelligence platform with deep analytics, enabling Truck Industry stakeholders to make decisions at their fingertips. Ashok Leyland was a challenger in FY 2020, but in FY 2026, it is now the market or segment leader in the MAV segment. The fleet owner prefers Ashok Leyland in the MAV segment because trucks can save 5 to 10% on fuel and AdBlue.

Tata Motors has launched a new range of trucks across various Rigid Haulage segments, offering additional payload capacity for fleet owners.

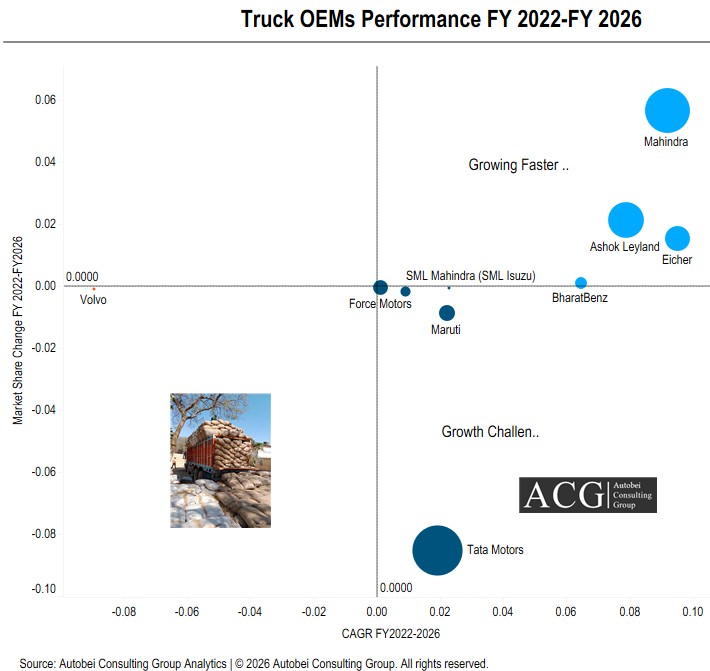

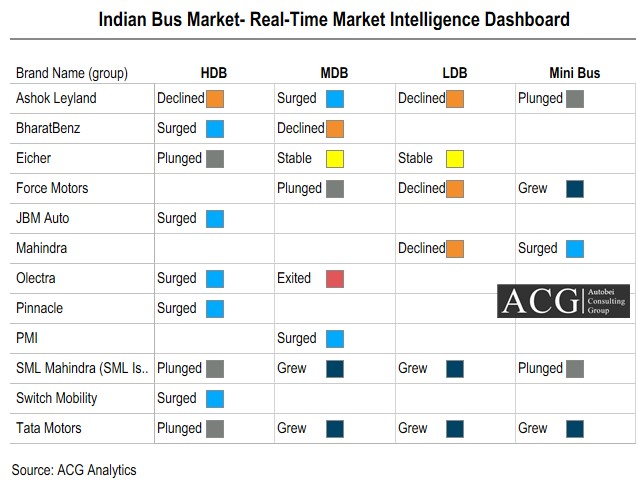

Market Share and Growth Analytics:

Tata Motors is a market leader in most of the truck segments in India. However, it is losing market share, or competitors are gaining market share due to changes in Product and market dynamics.

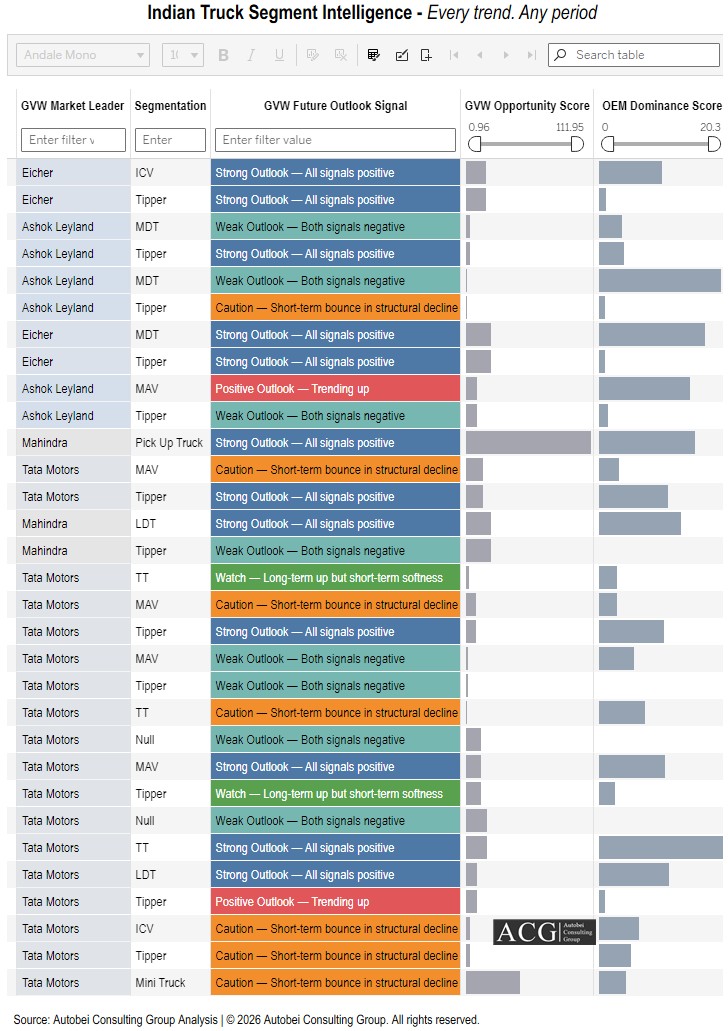

Indian Truck Market Segment-wise Forecast:

When OEMs want to launch a new product or model, the table below provides key insights for gaining market share in a specific segment. This partial part of the full analytics table. Tata Motors lost market share across 10 categories of the LDT, MDT, and HDT segments.

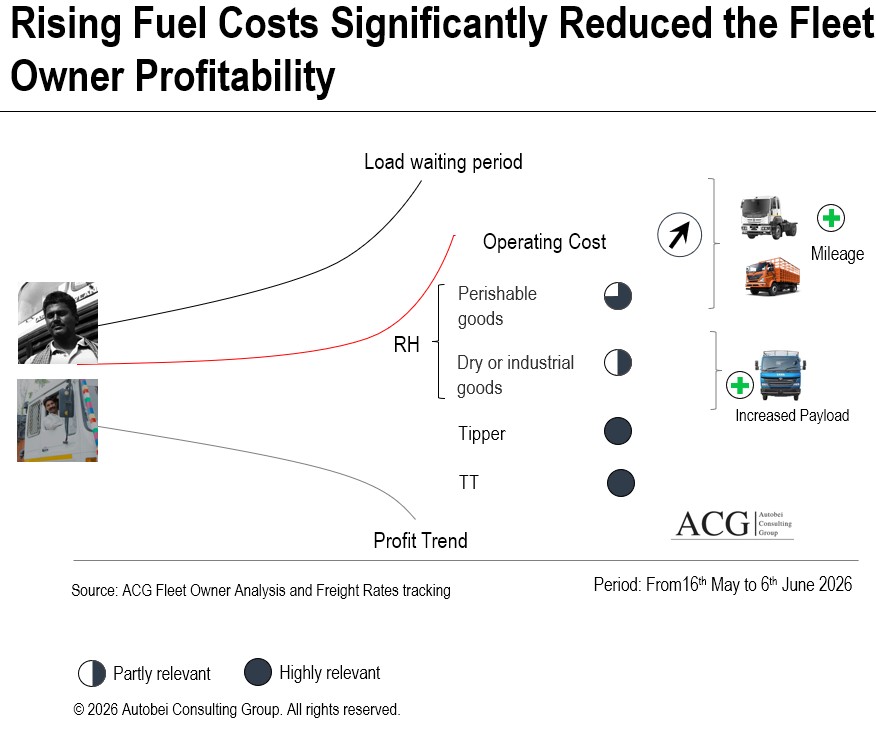

Impact of Fuel Price Increases on Fleet Owner Profitability:

The Truck Fleet owners have been facing a decline in profits over the last 1 year. After the fuel price increase in May 2026, there is a significant impact on operating costs and load demand.

The main segments that have been badly impacted are Tipper, Tractor Trailer, and Rigid Haulage, especially in Perishable goods transportation, where mileage plays a crucial role in profit.

Due to the high operating costs of Diesel Trucks, alternative fuel types like CNG and Electric Trucks will see strong growth in the coming months.

Contact us at Info@autobei.com to get the Full report

If the Digital platform works successfully, the Fleet owners’ revenue is expected to increase by 30 to 40% because truck utilization, reduced waiting period, and freight rates could also increase.

If the Digital platform works successfully, the Fleet owners’ revenue is expected to increase by 30 to 40% because truck utilization, reduced waiting period, and freight rates could also increase.